.svg)

AI is top of mind for many banking executives, and the number of AI applications across financial institutions continues to grow. While adoption has not matched some of the early ambitions, there is a clear sense of inevitability. The same trend is visible across nearly every aspect of consumer digital interaction, often progressing at an even faster pace. Chatbots are ubiquitous, ChatGPT ranks among the most visited websites, and Gemini summaries increasingly replace traditional clicks in Google Search.

The logical next step is to consider more customer-facing AI within retail digital banking channels. Financial services are uniquely suited for AI assistance: the data is already digital, it can be consolidated and interpreted, there is a clear ultimate metric (“$”), and processes are governed by well-defined rules and workflows.

Yet adoption is not happening at the pace one might expect. Partly, this reflects a broader reality that very few technological shifts occur quickly in banking. Unclear regulations and open questions around acceptable use and risk management do little to accelerate progress. Still, several strategies are emerging that are worth considering.

For many financial institutions, this appears to be the strategy of choice. While regulatory and operational blockers play a role, inaction is ultimately still a decision.

At many banks, digital channels exist primarily to enable access to services – and little more. We still live in a world where financial data is underutilized for personalization, and innovation cultures often struggle to gain traction. As a result, some institutions choose to wait or postpone investment. In certain cases, there is even a hidden sub-strategy: avoid doing anything customer-facing.

Behind the scenes, however, AI workflows and isolated tools are being adopted in the back office, largely in pursuit of operational efficiency. Very little of this progress reaches the end customer.

This remains a valid strategy, but it carries risk. Customer expectations may shift faster than banks are prepared to respond.

Prominent examples include Cleo and Plum. These are both chat-centric financial service providers frequently referenced by anyone exploring a holistic conversational experience. It is worth noting that each is supported by a focused, modern technology stack, and being “chat-first” is a deliberate strategy rather than an afterthought.

Customers appear to appreciate the experience, yet these apps often function as additions to everyday financial life. The primary account and main card typically remain elsewhere. Moreover, not everyone wants a chat-first interface, even if it is highly capable and intelligent.

Some form of chatbot is now standard for most financial institutions. Too often, however, these tools frustrate customers and are used mainly as a gateway to reach a human agent as quickly as possible. That said, some implementations are notably capable, with offerings from Bank of America, U.S. Bank, and Wells Fargo supporting a wide range of actions and insights.

The key challenge is recognizing that core utility (enabling tasks such as blocking a card, checking an account balance, or managing a budget) must function flawlessly. This is less an AI challenge and more an integration effort. Only once this foundation is in place does it make sense to introduce more advanced AI capabilities such as advisory services, analytics, and conversational support.

Making that leap is far from trivial. Advisory interactions differ fundamentally from workflow-driven tasks, and avoiding confusion for both the customer and the chat engine requires careful design.

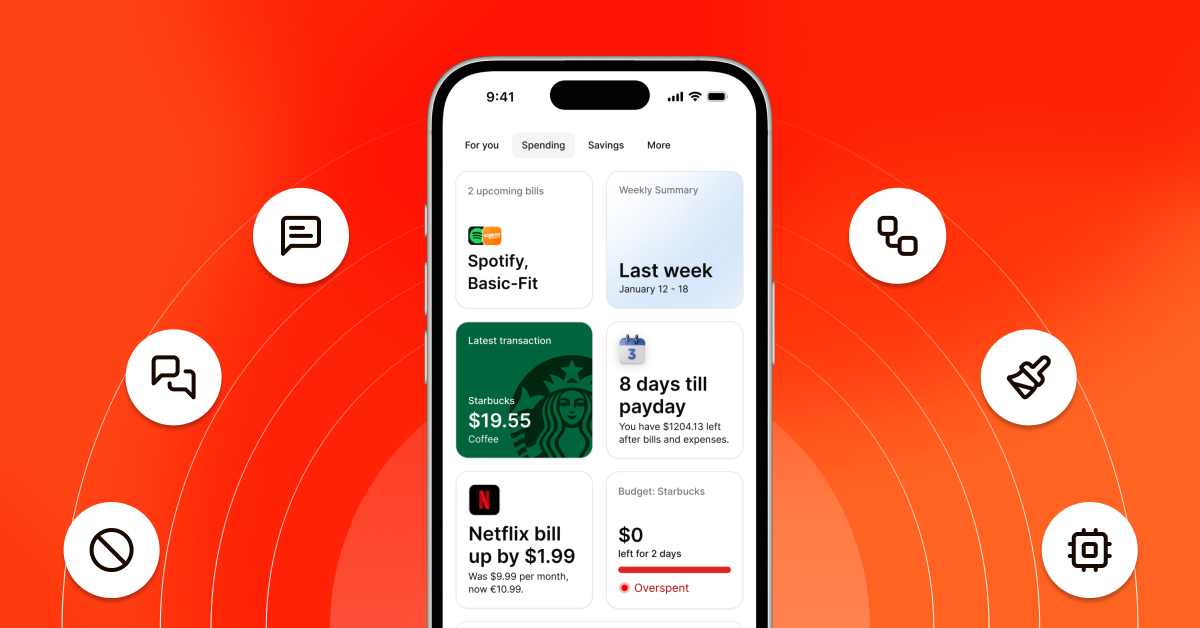

Not every experience requires AI (unless conversational AI is the only available interface). However, there are specific jobs where it can be exceptionally valuable: completing forms, providing tooltips or guidance, answering single-prompt questions, or summarizing documents, financial data, and past interactions. These are well-defined tasks where AI can truly excel.

The advantage of this approach is its ability to deliver tangible outcomes, such as higher conversion rates, improved customer sentiment, and lower servicing costs. The downside is the potential for a fragmented experience, where individual workflows lack awareness of what has occurred elsewhere.

Even so, this strategy has clear merits. A tightly controlled scope also provides a practical way to manage AI-related risks.

Though less visibly “AI-driven,” providing personalized content, from financial tips and insights to tailored offers, enables institutions to engage customers in a holistic and relevant manner. Given that banks already operate across multiple digital channels, introducing yet another channel (such as chat) risks unnecessary duplication unless it delivers genuinely new value.

A personalized, or hyper-personalized, approach allows financial institutions to improve experiences across the board. Because it relies on understanding customer data, combining it with relevant context, and identifying the right moment for engagement, it demands significant intelligence behind the scenes.

To customers, however, it may simply feel like their financial institution is finally delivering the relevance and accuracy they expect, rather than showcasing AI for its own sake.

Predictions about the death of the bank branch and the replacement of contact center agents with AI have circulated for years. Yet customers continue to value in-person, human experiences, and that preference may never fully disappear.

While maintaining human touchpoints is not always the most cost-effective option, the pursuit of efficiency is rarely as simple as shutting them down. Instead, equipping employees with AI tools to enhance that “last mile” interaction can be a powerful strategy, particularly in high-impact or emotionally sensitive scenarios.

Customer-facing AI in banking is no longer a question of if, but how. Institutions don’t need to pursue every strategy at once, but they do need a clear point of view on the role AI will play in their customer experience.

The organizations that succeed will be those that balance innovation with intention, focusing not just on deploying AI, but on solving real customer problems in meaningful ways.

If you're exploring how to bring AI into your digital banking experience — or want to move from experimentation to execution — now is the time to start the conversation. Get in touch to discuss how the right data, infrastructure, and strategy can help you deliver smarter, more relevant customer experiences.

___________________________

Customer-facing AI refers to artificial intelligence technologies that interact directly with bank customers. Common examples include chatbots, virtual assistants, personalized financial insights, fraud alerts, and AI-driven product recommendations.

Banks use AI to automate routine interactions, deliver personalized content, provide real-time financial guidance, streamline onboarding, and reduce service wait times. The goal is to make digital banking more intuitive, relevant, and efficient.

Yes, when implemented responsibly. Banks typically deploy AI within controlled environments, with strong governance, compliance oversight, and human review processes to manage risk and meet regulatory expectations.

Adoption is often limited by regulatory uncertainty, legacy technology infrastructure, integration complexity, and risk concerns. Many institutions are prioritizing back-office AI first before expanding into customer-facing use cases.

AI is expected to become a core layer of the digital banking experience, powering hyper-personalization, smarter servicing, and more proactive financial support. Banks that invest early in data and infrastructure will be better positioned to meet rising customer expectations.

Banks are exploring multiple paths to customer-facing AI, including chat-centric apps, side-channel assistants, embedded AI use cases, personalization strategies, and AI-supported human service. While progress is slower than in other industries, clear strategic choices (not experimentation alone) will determine success.

%201.webp)