.svg)

The Bud Breakdown is our way of demystifying complex topics across finance, data, and technology. Each edition takes a concept that’s often overused, misunderstood, or poorly explained, and breaks it down into clear, practical terms.

Our goal is simple: to make it easier for financial institutions to understand what really matters, why it matters now, and how it translates into better outcomes for customers.

In this edition, we’re looking at Personal Financial Management (PFM); what it actually means today, why it still matters, and how it needs to evolve to deliver real value in modern digital banking.

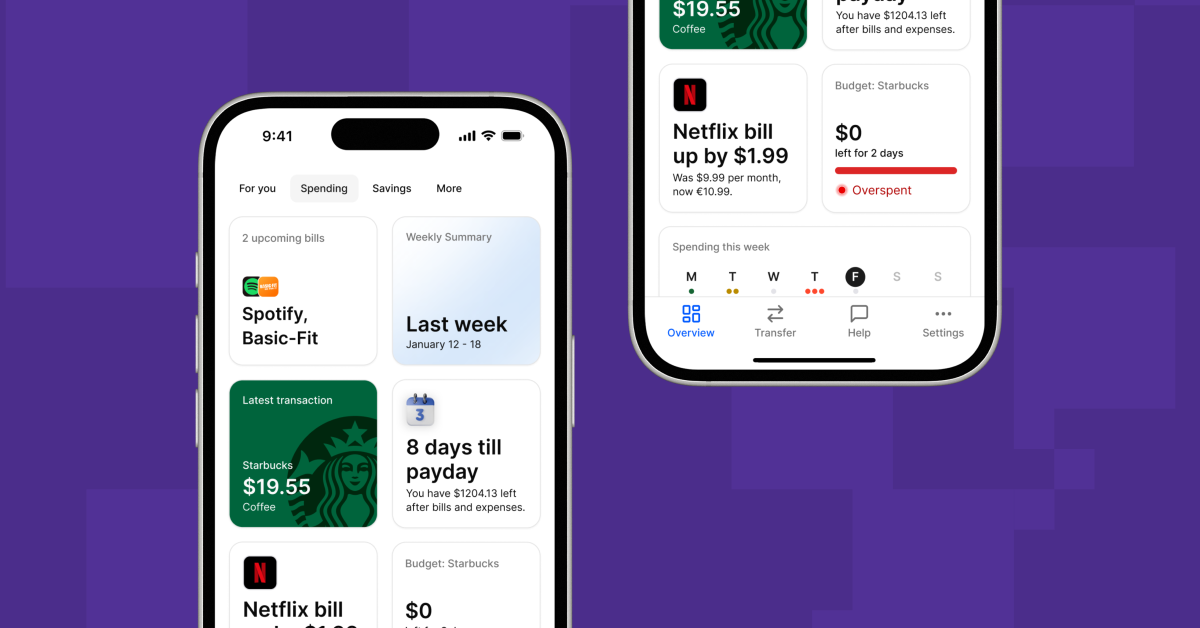

Personal Financial Management (PFM) refers to the set of digital tools and features that help customers understand, track, and manage their money within their banking experience.

The term itself dates back to the 1980s, emerging alongside personal computers and early financial software. Today, PFM has evolved into a broad umbrella covering everything from transaction insights and budgeting to goals, notifications, and financial guidance, all typically delivered through a bank, credit union, or fintech’s digital channels.

Despite decades of change in technology, the core objective of PFM has remained consistent: Capture financial data; Analyse and interpret it; and help determine next steps

From handwritten household budgets to spreadsheets to mobile banking apps, the goal is the same: help people get clarity and control over their finances.

In this article, we’ll look more closely at how that process works today, and whether traditional approaches to PFM are still fit for purpose in a modern financial landscape.

Across markets and demographics, improving personal finances — especially savings and financial security — remains one of consumers’ top aspirations. This is particularly pronounced among younger generations, who are more likely to set explicit financial goals. In fact, according to a 2025 Wells Fargo survey, nearly all U.S. adults planning a New Year’s resolution for 2026 are considering finances as part of their resolutions.

Yet despite this demand, many financial institutions still offer only basic digital experiences, with limited or poorly executed PFM capabilities.

The reason isn’t simply that “PFM doesn’t work” or that “customers don’t want it”. In reality, delivering a genuinely useful finance management experience is hard.

Key challenges include:

Together, these factors make PFM more important than ever. However, they also make it more complex to deliver well.

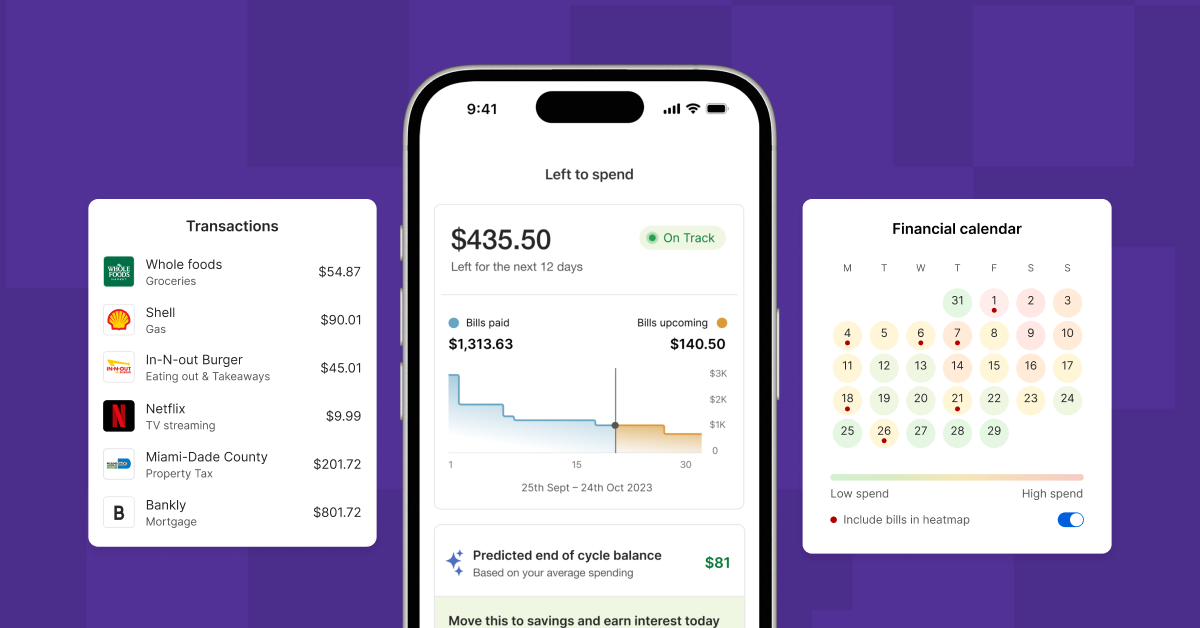

Every PFM experience starts with data. Open banking has made it easier to provide customers with a more holistic view of their finances, helping offset product fragmentation across institutions.

This enables foundational insights such as total available balance across accounts, liquid assets, or up-to-date income and spending views.

But raw data alone isn’t enough.

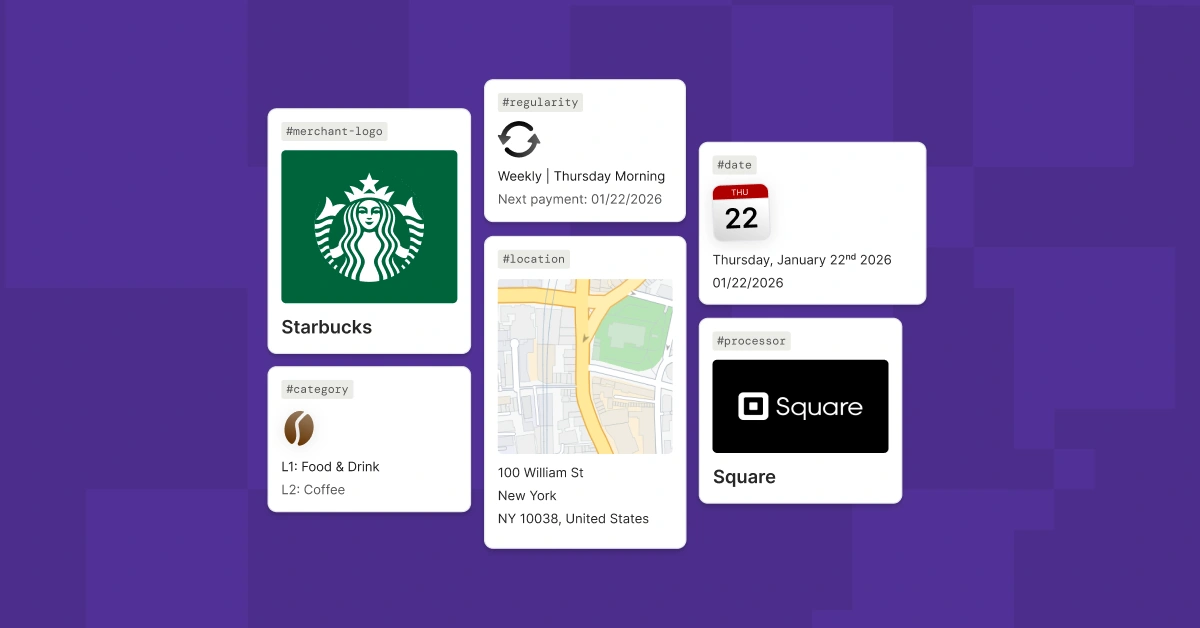

For financial data to be useful, it must be understood. Transaction enrichment is critical here: Transforming raw transaction strings into clear, meaningful information about merchants, categories, and context.

Without accurate enrichment, spend analysis breaks down, budgets become unreliable and insights lose relevance. Simply put, most PFM features depend on this layer. Without it, everything else struggles.

Once transactions are enriched, a range of category-dependent features become possible, including:

These features are largely retrospective, helping customers understand what has already happened. Useful, but not sufficient on their own.

Modern PFM must look forward, not just backwards. This includes:

Crucially, notifications should be actionable. It’s important to understand that action doesn’t always mean moving money. Sometimes, it’s simply prompting awareness or a mental adjustment (e.g. “you’re close to exceeding your budget”).

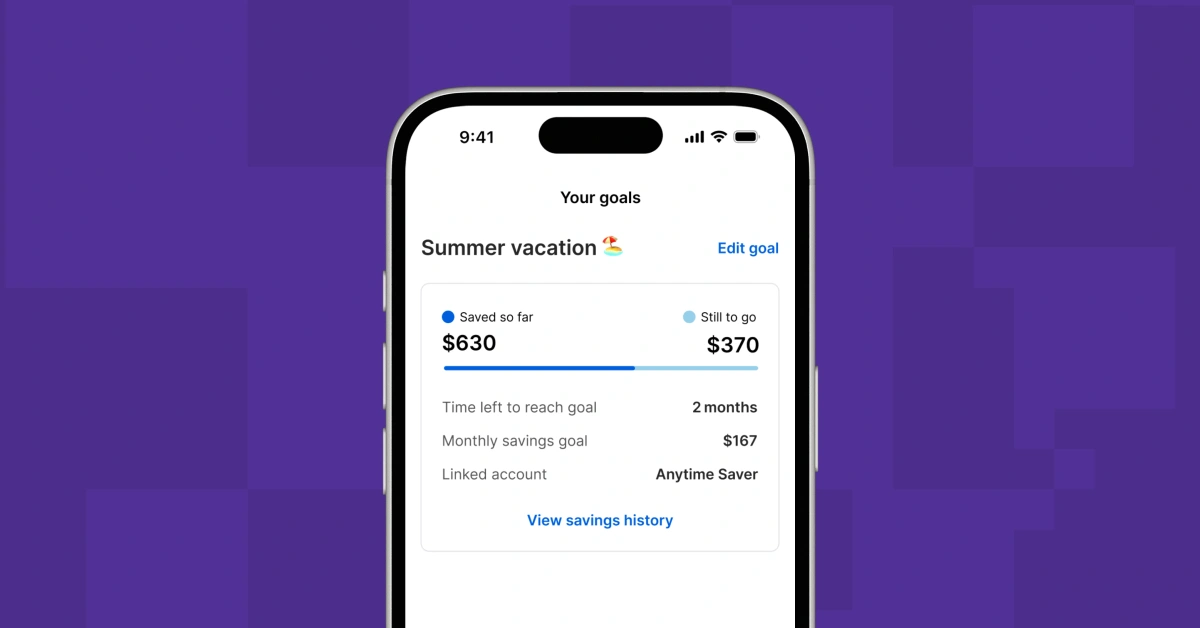

Goals, especially saving goals, are a central pillar of PFM, alongside mechanisms to get you there. These can take many forms:

Each mechanic aims to reduce friction and encourage positive financial behaviour, making them a natural part of a broader PFM experience.

PFM often overlaps with other areas, including:

While not always core, these features can enhance the overall experience when thoughtfully integrated.

The ultimate goal of PFM is to help customers improve their financial outcomes, but that only happens if customers are willing and able to engage.

Attention is scarce, and financial management competes with countless other priorities. This is where many PFM implementations fail, as they overwhelm users with features instead of focusing on relevance and timing.

Best practice PFM prioritises:

When done well, PFM has been shown to drive tangible outcomes, such as reduced overdraft usage and improved financial resilience.

Effective PFM isn’t just good for customers – it’s also strategically very valuable for financial institutions. Done right, it:

Importantly, improving customer financial outcomes and driving commercial results are not mutually exclusive. When insights are timely and personalized, both can coexist.

Almost every institution already provides some form of PFM; even a transaction list qualifies at a basic level. Rather than launching a separate, feature-heavy PFM section, it’s often more effective to enhance the existing transaction experience, layer in personalized insights, and meet customers in their day-to-day banking flows.

This approach avoids creating tools that only appeal to highly motivated “power users”.

PFM success depends on understanding each customer’s financial reality and its limitations. Key principles include:

Generic advice has little value when real-time transactional data and behavioural signals are available. Combining these intelligently drives relevance, engagement and, when appropriate, conversion.

Personal Financial Management has become a commodity feature in modern digital banking, but in many cases, it still fails to deliver on its promise.

Poor data quality, clunky interfaces, hidden features, and generic messaging all limit impact. In contrast, well-designed, seamlessly integrated PFM tells a clear financial story for each customer. When that happens, the results are better financial outcomes, happier users, and long-term value for the institutions that serve them.

Are you looking to integrate PFM features into your digital experience? Get in touch to find out how Bud can help.

_________________________________

PFM stands for Personal Finance Management. In banking, it refers to digital tools that help customers track spending, understand income, manage budgets, set financial goals, and gain insight into their overall financial position.

Common PFM tools include:

Most modern banks, credit unions, and fintechs offer at least a basic form of PFM.

PFM is important because it:

When delivered well, PFM helps institutions become a customer’s primary financial provider.

PFM can work, but only when it is built on high-quality data, accurate transaction enrichment, and relevant, timely insights. Feature-heavy or generic PFM tools often see low engagement, while personalised and proactive experiences are more likely to drive behavioural change.

Budgeting is a subset of PFM. While budgeting focuses on planning and controlling spending, PFM is broader and includes transaction insights, cashflow analysis, notifications, goals, and financial guidance.

Transaction enrichment transforms raw transaction data into meaningful information, such as merchant names, categories, and context. Without enrichment, spend analysis, budgeting, and insights are unreliable, making it one of the most critical components of effective PFM.

Open banking is not required, but it significantly improves PFM by enabling a more complete view of a customer’s finances across multiple institutions. When open banking data isn’t available, effective PFM should still adapt to the data that is available and personalise insights accordingly.

Modern PFM focuses less on static dashboards and more on:

The emphasis has shifted from “more features” to better timing and relevance.

PFM improves financial wellbeing by helping customers:

Small, timely insights often have a greater impact than complex tools.

Personal Financial Management (PFM) tools are designed to help customers understand, control, and improve their finances. While most banks and credit unions offer some form of PFM, many fail to deliver real impact due to fragmented data, generic insights, and poor engagement. When built on high-quality transaction data and delivered through timely, actionable insights, modern PFM can improve customer financial outcomes while driving engagement, trust, and long-term loyalty for financial institutions.

Product

Learn more about Bud's market-leading money management features

%201.webp)