.svg)

The institutions that win Gen Z today aren’t just acquiring customers; they are securing decades-long relationships.

Generation Z is already the largest generation globally, with spending power projected to reach $12 trillion by 2030, according to research from NielsenIQ, GfK, and World Data Lab. At the same time, a multi-trillion-dollar wealth transfer from Baby Boomers is accelerating their financial influence. Together, these forces represent one of the biggest growth opportunities the banking industry has seen in decades.

But capturing this segment requires more than competitive rates or polished branding. To understand how banks should respond, it helps to first understand what makes this generation fundamentally different.

Gen Z approaches money with a mix of caution and urgency that is reshaping expectations of financial institutions.

More than 80% say their finances contribute to stress, and nearly half report that they do not feel financially secure in 2025, a sharp increase year over year according to Deloitte. In a recent YouGov survey, only 35% of Gen Z respondents said their income allows them to save each month, while 23% struggle to cover expenses. Unsurprisingly, 70% say they are more careful with money than they used to be.

For banks, this signals a clear shift: Financial wellness tools are no longer a differentiator. Instead, they are a baseline expectation for younger generations. Embedded financial guidance inside the banking experience is becoming critical, and customers want help making smarter decisions in real time, not after the fact.

Yet support alone is not enough. Gen Z expects banks to understand them on an individual level.

Having grown up in a digital-first world characterized by algorithm-driven playlists, tailored shopping suggestions, and hyper-relevant content feeds, it is perhaps no shock that Mastercard research shows that Gen Z values personalization significantly more than the average consumer. Meanwhile, 72% say they want banking experiences tailored to their goals starting at onboarding.

Many institutions claim personalization, but too often it relies on demographic segmentation that assumes people with similar incomes or ages behave the same way. That approach falls short with a generation whose financial lives are highly dynamic.

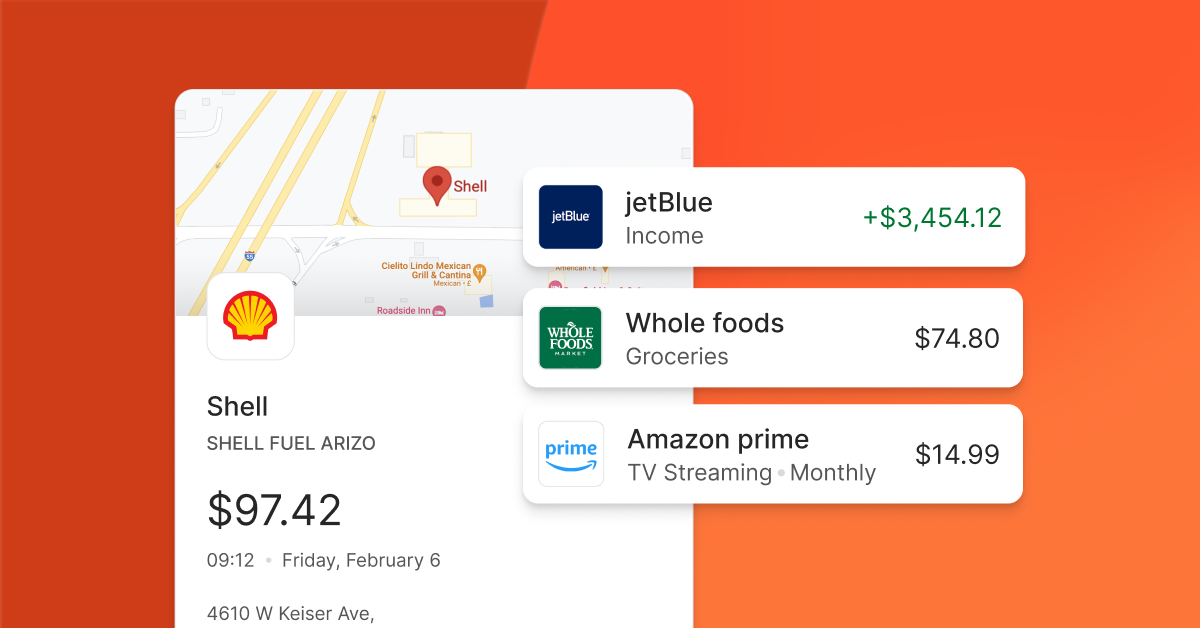

But you cannot personalize what you cannot interpret. True personalization starts with understanding customer behavior at the transaction level instead of guessing based on static attributes. This is where enriched data becomes foundational. With Bud’s Enrich, banks can transform raw transaction data into actionable insight through:

When institutions have this level of clarity, they can deliver experiences that feel genuinely helpful rather than generically targeted. And when relevance is missing, Gen Z is quick to respond by moving elsewhere.

Research from PYMNTS shows that Gen Z switches banks two to three times more often than their parents and four times more than their grandparents. At the same time, roughly half say they would consider switching to a community bank, online-only institution, or credit union, according to Apiture. This creates a meaningful opening for smaller institutions that are prepared to meet modern expectations.

Retention has become an experience problem rather than a pricing problem. Community banks and credit unions can compete effectively, but only if they deliver digital engagement that matches or exceeds what younger consumers see elsewhere.

Which brings us to where Gen Z actually lives: mobile.

For 66% of Gen Z, the mobile app is their primary way to bank. More than half cite digital capabilities as a top factor when choosing a new institution, and 78% maintain just one bank account according to YouGov. In practice, this means the primary app captures the majority of engagement. In other words; if your app is not sticky, it is replaceable.

Leading institutions are responding by evolving their apps from transaction hubs into intelligent financial companions, but delivering that level of intelligence starts with data.

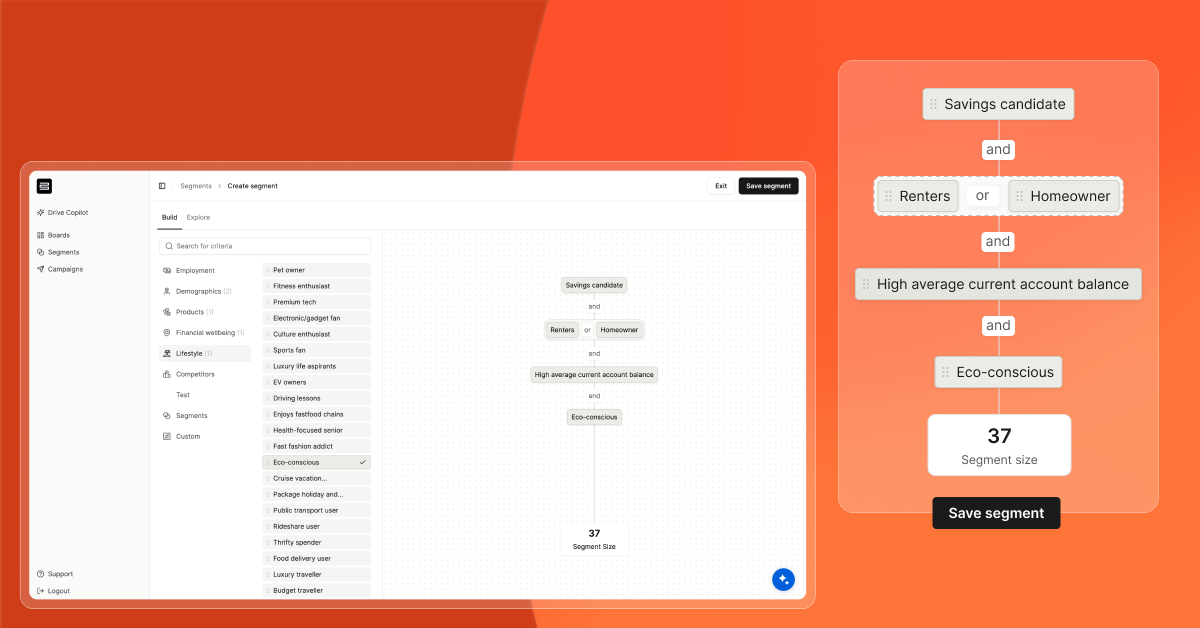

Bud’s Drive product helps financial institutions activate the vast amounts of transaction data they already hold by transforming it into AI-powered, actionable insights that teams across the organization can use without technical expertise. With ready-made segments and real-time intelligence, banks can better understand their accountholders, identify growth opportunities, and anticipate customer needs.

Instead of relying on broad campaigns or static segmentation, institutions can engage customers with personalized messaging, support, or product recommendations that feel timely and relevant. Whether highlighting accountholders who may be ready to start saving, identifying those drifting toward financial stress, or surfacing customers underserved by competitors, Drive enables financial institutions to create interactions that clearly communicate, “we understand you.”

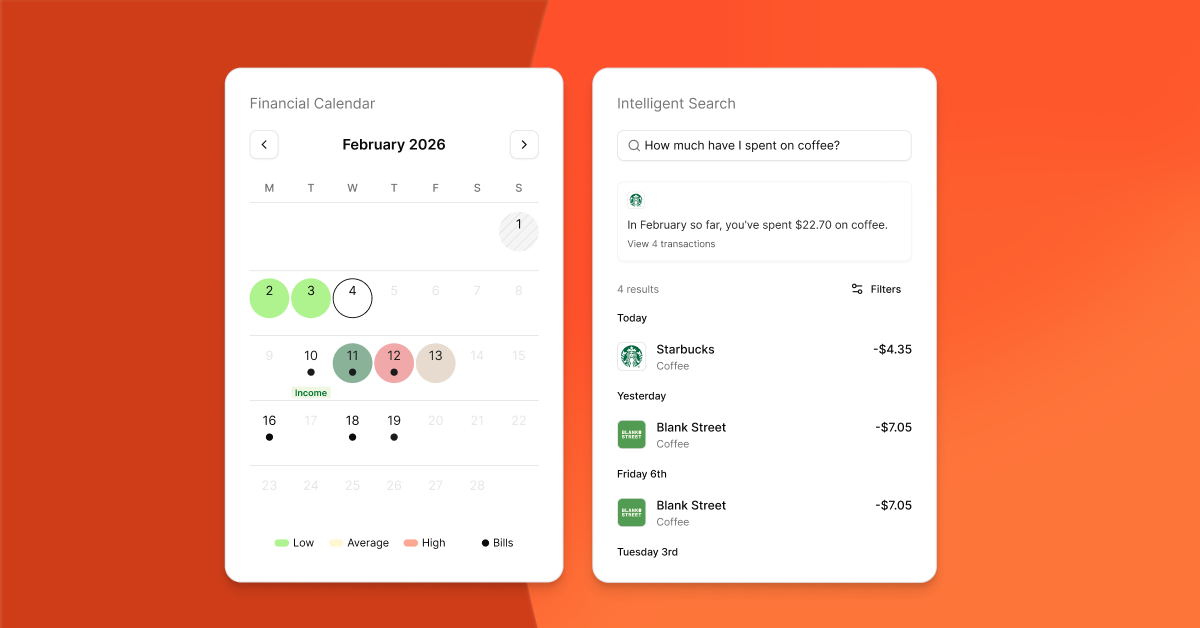

Institutions can then surface these insights to their accountholders through Bud’s Engage product. Combined with our highly accurate enrichment capabilities, Engage allows you to deliver engagement-driving customer banking experiences that drive deposits and savings with:

Engage also uses embeddable front-end PFM widgets that make customer experience easy. Capabilities include:

Together, these features can help Gen Z customers stay oriented, confident, and in control, all within the banking app they already use – which, as we covered previously, is one of the most important factors for this segment.

Gen Z is not looking for more tools, necessarily. Rather, they are looking for effortless financial progress. Consider that 73% of teens say they want more personal finance education, while 52% worry about financial stability (Mastercard, 2025). The opportunity for banks is clear: translate complex financial data into simple, actionable guidance.

The strongest engagement strategies do not demand more attention from users. They reduce cognitive load and simplify decision-making. When executed well, the impact is significant:

Over time, this is what transforms a primary account into a primary relationship.

The macro stakes are difficult to overstate. A $12 trillion spending trajectory. A historic wealth transfer. A generation defined by low loyalty and high expectations. All that is to say, waiting is the biggest risk.

Gen Z is forming primary banking relationships now, and once financial habits are established, switching behavior typically declines with age. The institutions that engage now have a powerful advantage. This generation is not asking banks to reinvent themselves entirely – instead, they are asking them to become genuinely helpful. With enriched data powering personalization and embedded engagement turning insight into action, financial institutions can move beyond servicing accounts and begin building financial confidence at scale.

The question is not whether Gen Z will reshape banking. It is whether your institution will be ready when they do.

Get in touch to learn how Bud’s solutions can help you deliver the personalized, insight-driven experiences that today’s customers expect — and build relationships that last for decades.

___________________________

Gen Z is the largest generation globally and is projected to control $12 trillion in spending power by 2030. As they form primary banking relationships now, institutions that engage them early have an opportunity to build decades-long customer loyalty.

Gen Z expects personalized, mobile-first banking experiences that provide real-time insights, financial guidance, and tools that help them make smarter money decisions. Relevance and ease of use are critical to earning their trust.

Personalization allows financial institutions to deliver timely recommendations, tailored product offers, and meaningful financial guidance. Without it, experiences can feel generic, increasing the likelihood that customers switch providers.

Banks can personalize at scale by activating transaction data to better understand customer behavior. Enriched data and AI-powered insights make it possible to anticipate needs, segment intelligently, and deliver relevant engagement across digital channels.

Transaction data provides the foundation for understanding spending patterns, financial habits, and customer intent. When transformed into actionable insights, it enables banks to create proactive experiences that deepen relationships and increase product adoption.

To win Gen Z, banks must combine strong digital experiences with personalized financial support. Mobile-first design, embedded financial wellness tools, and insight-driven engagement help institutions remain relevant and build long-term trust.

Gen Z is poised to become the most valuable customer segment in banking, but winning them requires more than traditional digital experiences. Financial institutions must deliver personalized, insight-driven engagement powered by enriched transaction data. By activating customer intelligence with Drive and surfacing it through Engage, banks can turn their apps into proactive financial companions; building trust, deepening relationships, and securing lifelong customers.

%201.webp)