.svg)

An LLM without a broad context about a customer's actual financial life is a chatbot.

An LLM that knows who that customer is, what they've done across every product, what's about to happen in their life, and which actions historically work for people like them. That's an agent.

The difference isn't the model. It's the layer underneath. And almost nobody in financial services is saying this loudly enough.

The AI conversation in banking has been consumed by the agent layer. Which model, which copilot, which use case, which vendor, who just partnered with whom? But agents are only as good as the data and intelligence they stand on, the data inside most banks is in no shape to be reasoned over.

Banking is at the start of a generational infrastructure shift. The institutions that win the next decade won't be the ones with the loudest AI announcements. They'll be the ones that quietly built the right foundation while everyone else was buying chatbots.

Banking has been through this before. The mainframe generation. The digital generation. The mobile generation.

Each one required banks to add a new layer to the stack. Each time, the institutions that built the right layer at the right moment pulled ahead and the ones that didn't ended up renting the capability from challengers who built it first. Once the wave passes, the internal political will to start again disappears. This is why speed matters.

We're now at the start of another one. Call it the agentic banking generation: software that doesn't just summarise statements or answer FAQs, but acts on a customer's behalf. Picks the right product. Picks the right moment. Runs entire workflows that used to take an internal team a quarter to plan.

But you can't agent your way out of an ontology problem.

Walk into any large bank's data org and you find the same picture. A core banking system with transactions and balances. A CRM with relationship data. CRA data. Product systems, channel data, marketing platforms, KYC, credit bureau pulls. A warehouse someone built five years ago that nobody fully trusts.

Every one of these systems was built for a specific purpose, by a specific team, with its own conventions. Customer IDs don't line up. Transaction descriptions are inconsistent garbage strings. Two systems regularly disagree about basic facts, like a customer's address. The bank has no shared definition of who a customer even is.

Eighteen months ago I was reading reports of thousands of AI trials inside banks. When I interviewed Simon Taylor, he told me: "they will all fail." I cautiously agreed. For execution reasons. Today I agree for a different reason.

When a bank tries to do something genuinely AI-native on top of this stack, "tell me which of my customers are at risk of attrition in the next 90 days and what we should offer them", they hit the wall. Not because the models can't do it. Because the data underneath is unreasonable.

The question for the next five years isn't which LLM we should use. It's how good is the intelligence layer everything else plugs into?

This isn't a banking-only story. The most interesting AI companies of the last two years aren't horizontal LLM wrappers. They're vertical intelligence layers, each solving the same shape of problem in their industry.

In legal, Harvey and Legora aren't ChatGPT for lawyers. They're the layer that connects a firm's documents, precedents, and case data and exposes it to drafting tools, research agents, and review workflows. Without that layer underneath, you get a chatbot that hallucinates citations.

In healthcare, Abridge sits between the clinical conversation and the EHR, turning ambient audio into structured data that becomes the foundation for billing, documentation, and downstream workflows. OpenEvidence has become the medical-knowledge layer clinicians query in real time.

Palantir is the cleanest example of all. Foundry and Gotham are explicitly the operational data layer for organisations whose data is scattered across legacy systems. Every analysis, dashboard, workflow, and agent built on Palantir runs against the ontology Palantir provides. It is the most quoted, most copied version of the intelligence-layer thesis in software.

Sierra and Decagon have made the same point in customer service: two AI companies with identical models can have wildly different performance depending on how well they've structured the layer underneath.

The lesson is the same everywhere. In any industry where the data is messy, regulated, and high-stakes, you need an intelligence layer for AI to safely deliver on its promise.

Banking is the messiest, most regulated, and highest-stakes vertical of all (warfare excepted). The layer matters more here than anywhere.

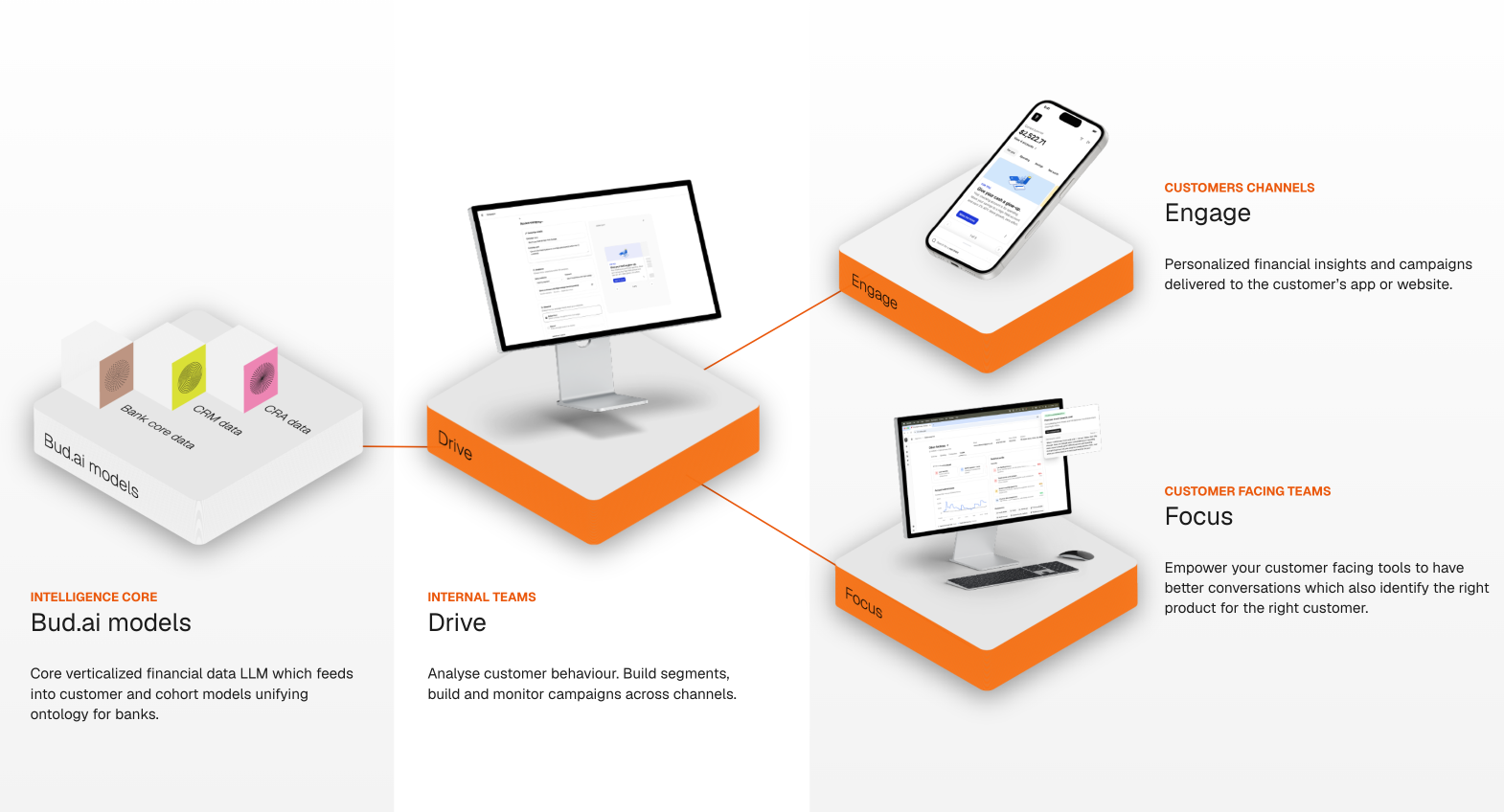

Bud is the customer intelligence layer for financial services.

We sit across a bank's data assets, core banking, CRM, CRA, product systems, channel signals, turning it into something the bank can actually reason over.

We connect to the systems banks already run, meeting the data where it actually lives rather than where the architecture diagram says it should.

We enrich and model that data with years of accumulated work on financial-specific problems: transaction categorisation, merchant resolution, income and expense detection, life-event prediction, financial-health scoring, product propensity, and attrition risk. Generic AI doesn't do this. It takes deep, financially-literate modelling with the labelling, edge cases, and regulatory rigour the industry demands.

We expose all of it as a coherent intelligence layer any team, product, or agent can query. Unlike tools built twenty years ago that are now bolting on APIs and calling themselves "headless," Bud was architected from day one to power agents.

That's the platform. It's what every bank needs to participate in what's coming next. It's also the part that is hardest to build internally.

Once the layer exists, the question becomes what you build with it. We've shipped three products that show what's possible.

Drive. Analyse and segment your customers in one place or, let Drive Agent do it for you. Define a cohort in seconds. Push the right message or product to the right customer at the right time, through the bank's existing stack or into Focus and Engage.

Focus. Customer intelligence for front line teams. Relationship managers, sales teams, and customer support get a clear picture of a single customer they are speaking with. This customer just had a life event. Here's the product to offer. Here's the conversation to have. Here's the one-click action to make it happen. We see huge cross-sell uplift here, especially in teams that have never been empowered to sell.

Engage. Intelligent customer-facing tools, APIs, and embeddable widgets that create hyper-personalized experiences in a bank's app and website. Next best action, in real time, controlled centrally from Drive.

Drive, Focus, and Engage show what becomes possible. They are not the whole story.

There are a dozen high-value workflows inside every bank. Fraud and risk. Lending. Financial wellbeing. SMB treasury. Collections. Onboarding. Retention. Every one of them is a candidate to be built on top of the intelligence layer.

We won't build all of them. We shouldn't.

So we give our our clients a choice:

This is the right shape for an AI platform in a regulated industry. A durable core. Applications above it built by vendors, customers, and partners alike. Trying to be the only thing that runs on your own platform is how vertical AI companies end up shipping mediocre products in too many directions.

Making the agentic banking generation happen is not just end LLM deployment is. It's about having centralized intelligence or ‘source of truth 2.0’ which isn’t a black box but is verifiable and auditable layer to allow Ai applications to perform.

Until every team, every product, every agent, and every customer-facing experience inside a bank works from the same understanding of who its customers are and what they need — the AI conversation in financial services stays stuck in demo.

That layer has to exist. It has to be purpose-built for financial data, not adapted from a horizontal tool. It has to be deployable with the regulatory and operational rigour this industry demands.

We've spent ten years building it. Now is the moment to say so out loud.

Every bank in the world is about to make this decision, whether they realise it or not. They will either build the layer themselves, buy one that was made for them, or rent the capability from a challenger who got there first. The third option is how the last three generations of banking technology played out. We don't think it has to play out that way again.

If you run a bank, fintech or AI platform and you've hit the wall, come talk to us. The next decade of banking will be built on top of the intelligence layer. Let's make sure you're building on the right one.

%201.webp)