.svg)

Hyper-personalization is one of the most talked-about concepts in retail digital banking, but it’s also one of the most misunderstood. Often dismissed as a buzzword, the reality is far more transformative.

In this Bud breakdown, we explore what hyper-personalization really means, how it’s enabled, why it matters to financial institutions, and what the journey toward delivering it actually looks like.

Hyper-personalization is the ability to use modern technology and customer data to deliver highly individualized experiences at scale.

Every financial institution already provides some level of “personal” experience; customers can view their own balances, transactions, and products. But true hyper-personalization goes much further. It introduces a proactive, granular approach that anticipates customer needs, surfaces relevant insights, and enables timely action.

For decades, banks relied on demographic segmentation built from easily accessible data such as age, income bracket, or ZIP code. While useful, these segments offered only a partial view of the customer.

Today, two major shifts have changed what’s possible:

Hyper-personalization sits at the intersection of these shifts. However, having detailed data or real-time infrastructure alone isn’t enough. Delivering a true “segment of one” experience requires an intelligent decisioning layer: a “brain” capable of interpreting signals, understanding context, and determining the best next action.

Technology is the primary enabler of scalable hyper-personalization. Advances in AI, machine learning, and real-time data processing allow financial institutions to move beyond isolated, highly tailored moments toward continuously optimized customer experiences. But advanced analytics are only as effective as the data that powers them.

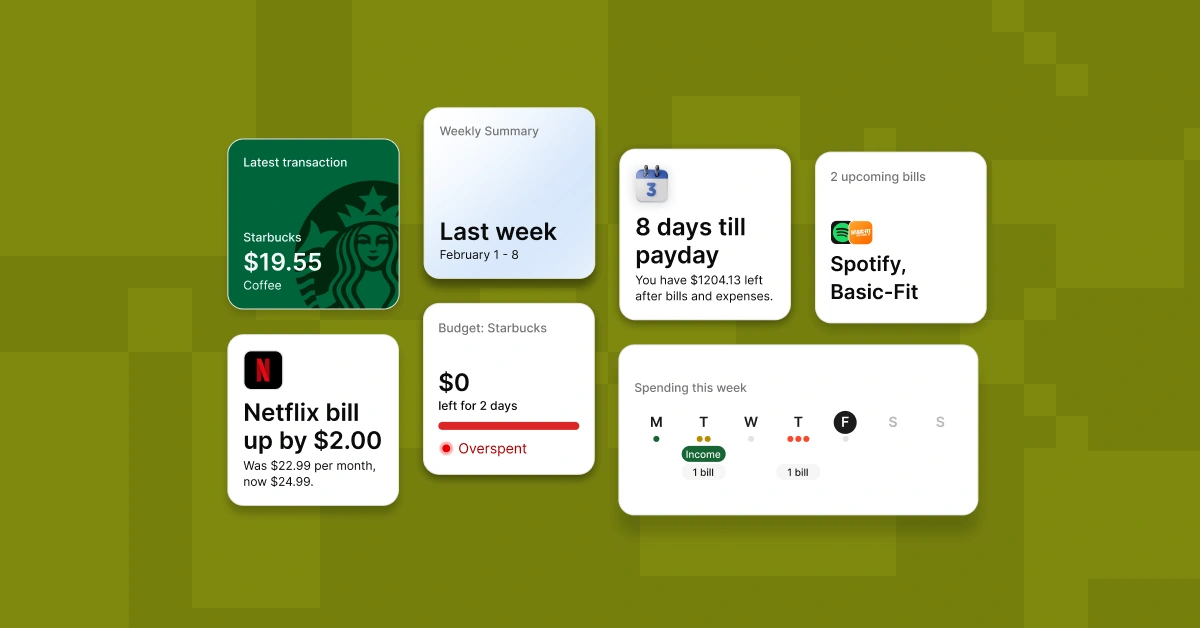

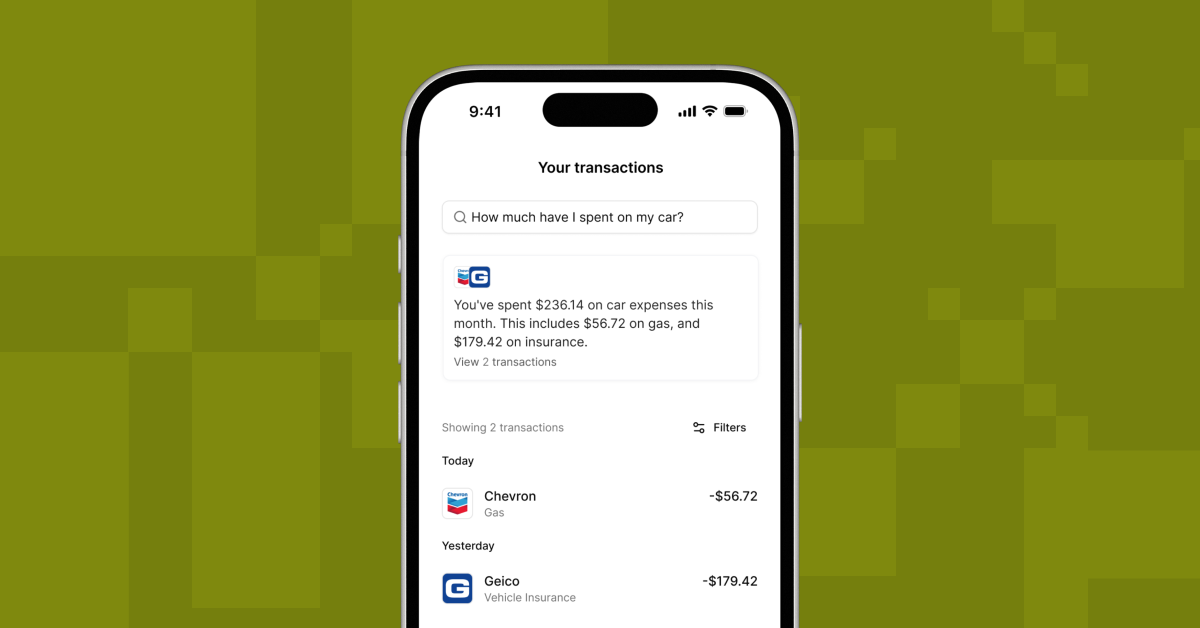

High-quality transaction data is foundational. Financial transaction enrichment (transforming raw transaction strings into structured, meaningful data) is arguably the single most important ingredient. Without it, understanding customer behavior at a granular level becomes nearly impossible.

Additional data sources further enhance decisioning by:

AI-driven analytics make it possible to move from “occasional hyper-personalization” to a world where, for every customer, the best message, action, or offer is evaluated at any given moment.

The availability of technology doesn’t automatically create demand, but in this case, demand already exists. Consumers are accustomed to personalized experiences across digital marketplaces, search engines, and travel platforms. Relevance is now the default expectation. That expectation extends to financial services.

Research consistently shows that personalization plays a significant role in provider selection and overall satisfaction. Compared to many other industries, banks are uniquely positioned to deliver hyper-personalized experiences due to the depth of financial data they hold, the longevity of customer relationships, and the trust they’ve built.

The evidence is clear: hyper-personalization benefits both customers and financial institutions.

This means that hyper-personalization is actually a legitimate growth strategy for the financial institution, and not just a customer experience initiative.

At Bud, we believe our role in the hyper-personalization story is central: It starts with data. Our AI platform is a market leader in understanding financial behavior, enabling institutions to build accurate, actionable views of every customer. These insights can be shared across existing systems, amplifying the value of prior technology investments.

Bud also provides an integrated suite that supports the full digital customer lifecycle:

Together, these capabilities enable hyper-personalization across every channel. A strong example is Intelligent Search; a feature that combines powerful transaction search, AI-generated summaries, contextual notifications, and relevant offers triggered by customer behavior.

Moving toward hyper-personalization doesn’t require a full-scale transformation overnight. Most institutions begin with focused use cases — small but meaningful moments of relevance — and expand from there. Common starting points include:

As capabilities mature, consistency across channels becomes increasingly important, ensuring customers experience a single, coherent relationship rather than disconnected interactions.

Hyper-personalization is quickly becoming table stakes, but its long-term significance goes further.

The infrastructure required to deliver real-time, AI-driven experiences also enables more autonomous, agent-led banking models. Institutions that invest now are futureproofing their organizations, as well as unlocking immediate value.

Ignoring this shift risks more than missed revenue opportunities. It risks falling behind in a market where relevance is fast becoming the primary competitive advantage.

Bud helps banks, credit unions, and fintechs turn customer data into intelligent, real-time experiences that drive measurable impact. Talk to our team to explore how we can help you activate your data and deliver the right insight, message, or offer at exactly the right moment.

________________

Hyper-personalization uses AI, real-time data, and advanced analytics to deliver highly tailored financial experiences to individual customers at scale.

Traditional personalization relies on broad customer segments. Hyper-personalization treats each customer as a “segment of one,” using behavioral data and contextual signals to determine the best next action in real time.

It improves customer satisfaction, increases product adoption, reduces cost to serve, and strengthens long-term loyalty while helping institutions stay competitive.

Key components include enriched transaction data, AI and machine learning models, real-time processing, and intelligent decisioning platforms.

No. Many begin with targeted use cases, such as personalized insights in money management tools or AI-assisted branch conversations, and scale gradually.

Hyper-personalized experiences are becoming the default. The same capabilities will soon support autonomous financial guidance and agent-driven banking models.

Hyper-personalization enables financial institutions to deliver individualized experiences at scale by combining enriched transaction data, AI, and real-time decisioning. As customer expectations for relevance continue to rise, banks and credit unions have a unique opportunity to use their data advantage to provide proactive insights, improve satisfaction, reduce cost to serve, and drive growth. With the right technology foundation, hyper-personalization doesn’t require a full transformation. Institutions can start small, scale strategically, and future-proof their customer experience.

%201.webp)