.svg)

Your customers' transactions are a running record of their financial lives. Every direct deposit, subscription charge, and point-of-sale swipe is a signal. Together, they tell a story about what someone earns, what they owe, what they're building toward, and where they're struggling.

Most banks aren't reading that story. Not because the data isn't there, but because it's raw, siloed, and hard to act on at scale. The institutions that are starting to use it aren't just seeing incremental gains; they're identifying opportunities and risks that simply weren't visible before.

Here are eight of the most surprising things transaction data can tell you, and what banks are doing with them.

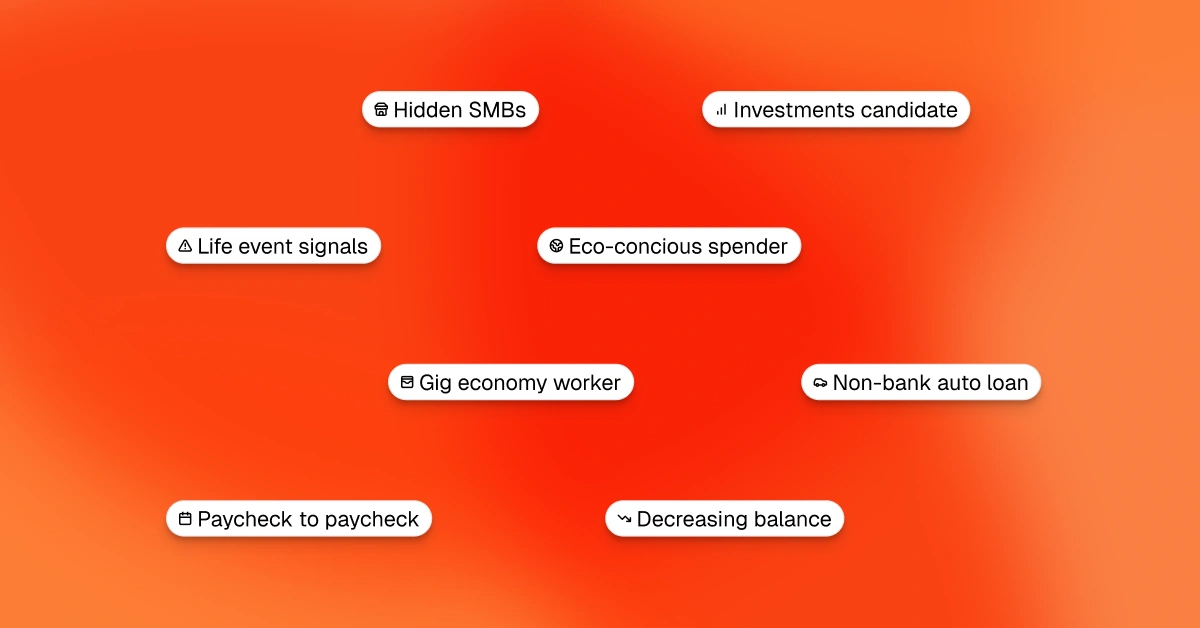

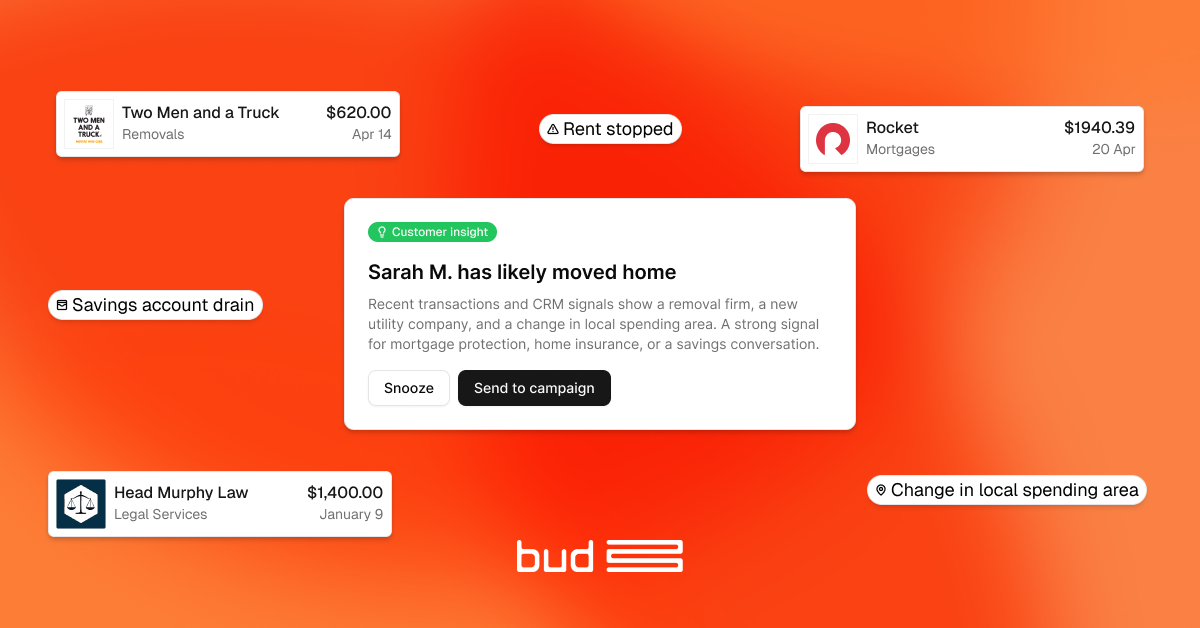

Life events are among the highest-converting moments in retail banking. A customer who has recently moved home, started a new job, or come into a significant windfall is far more receptive to a relevant product conversation than someone receiving a generic campaign.

The problem has always been timing. By the time a credit bureau refreshes or a customer fills out a form, the window has often closed. Transaction data moves faster. A pattern of removal van hire, utility setup payments, and new local merchant spend tells you someone has moved, often within days of it happening. A sudden large deposit indicates a windfall. A shift in income source signals a job change.

Bud instantly surfaces these events, so product teams can reach the right customer at the right moment; before a competitor does.

A meaningful share of personal account holders aren't just consumers; they're actually running businesses through their personal accounts. They're taking Stripe payouts, paying contractors, subscribing to business SaaS tools, and receiving settlements from Shopify or Square.

Most banks don't know they're there. The account seems to be retail. The transactions look like noise. But once you know what to look for, the pattern is clear.

Bud identifies these customers from their transaction signals (payment processor inflows, payroll-style outflows, multi-platform income, business software spend), and flags them as high-probability business banking leads sitting inside your existing book.

Converting even a fraction of them into proper business accounts unlocks merchant services, SMB lending, commercial cards, and significantly higher lifetime value. Every one of them is currently using a fintech to fill a gap you haven't spotted yet.

The gig economy and creator economy are not new, but the banking infrastructure built to serve them largely hasn't caught up.

Traditional income verification was designed for W-2 employees with predictable, single-source pay. It systematically fails freelancers, platform workers, and creators; people earning from Etsy, Substack, YouTube, Uber, and a dozen other sources simultaneously.

Bud maps income at the platform level; not only "freelance" as a broad category, but specifically: Shopify payouts, Etsy deposits, Stripe settlements, DoorDash earnings. That granularity changes what's possible. It enables genuine underwriting for a segment that most institutions currently turn away. It also opens the door to genuinely tailored products: income-smoothing tools, business debit cards, tax-aware savings.

The banks that move early here won't just acquire customers, they'll define what creator banking looks like before the fintechs consolidate it.

Age and postcode are proxies. Useful ones, historically, because we didn't have anything better, but in reality they're only partial predictors of what a customer actually needs or wants from their bank.

Knowing that someone shops consistently at premium grocers, takes three international flights a year, and recently started spending at EV charging stations tells you something genuinely useful. It tells you how they see themselves, what they value, and what kind of financial products are likely to land.

Bud applies hundreds of behavioural flags out of the box, from "eco-conscious spender" to "frequent flyer" to "fast fashion shopper" to "fitness enthusiast." Instead of just being demographic proxies, these are derived directly from what customers do with their money.

For marketing teams, that's the difference between a segment called "millennials" and a segment called "affluent eco-conscious travellers".

Consumer Duty and financial resilience expectations have raised the bar. It's no longer enough to have a vulnerability policy, as regulators want evidence that institutions are actually identifying customers in difficulty and acting on it proactively.

Transaction data is where those signals live. Gambling spend as a proportion of income. Debt-to-income ratios derived from real cash flows. Frequency of NSF (‘not sufficient funds’) events. The proportion of income that never makes it past day three of the month. Bud builds these indicators directly from transaction behaviour, with enough resolution to be genuinely useful — paycheck-to-paycheck bands, for instance, are tracked in 5-point increments, not broad buckets. The output is explainable, auditable, and designed to be acted on, by a compliance team interrogating the methodology or a frontline colleague having a difficult conversation.

Most cross-sell programmes follow the same basic pattern: pick a product, build a list, run a campaign, wait, measure, repeat. It's slow, it's often based on stale data, and it requires significant effort to get right.

Bud inverts this. Rather than starting with a product and finding customers, it starts with customer behaviour and surfaces product candidates automatically. "High income, no savings" is a savings product conversation. "Business spender without a business card" is a commercial card lead. "First-time homebuyer candidate" is a mortgage discussion. These aren't built manually, but rather update continuously as customer behaviour shifts.

For a team running next-best-action models, the difference is significant: instead of working from lists built last quarter, you're working from signals that reflect what customers are doing right now.

Attrition is rarely sudden. Customers drift before they leave; balances decline slowly, salary deposits start going elsewhere, spending on your card reduces while increasing on a competitor's. By the time a customer formally churns, the signals were there months earlier. The same is true of credit risk — a business customer whose income is declining quarter on quarter is a collections risk that's far better managed early.

Bud flags these trajectories automatically: decreasing balance, high proportion of income transferred out, lapsed saver, savings drainer, declining business income. These become trigger events. Not lagging metrics reported after the fact, but instead leading indicators that retention and risk teams can actually act on.

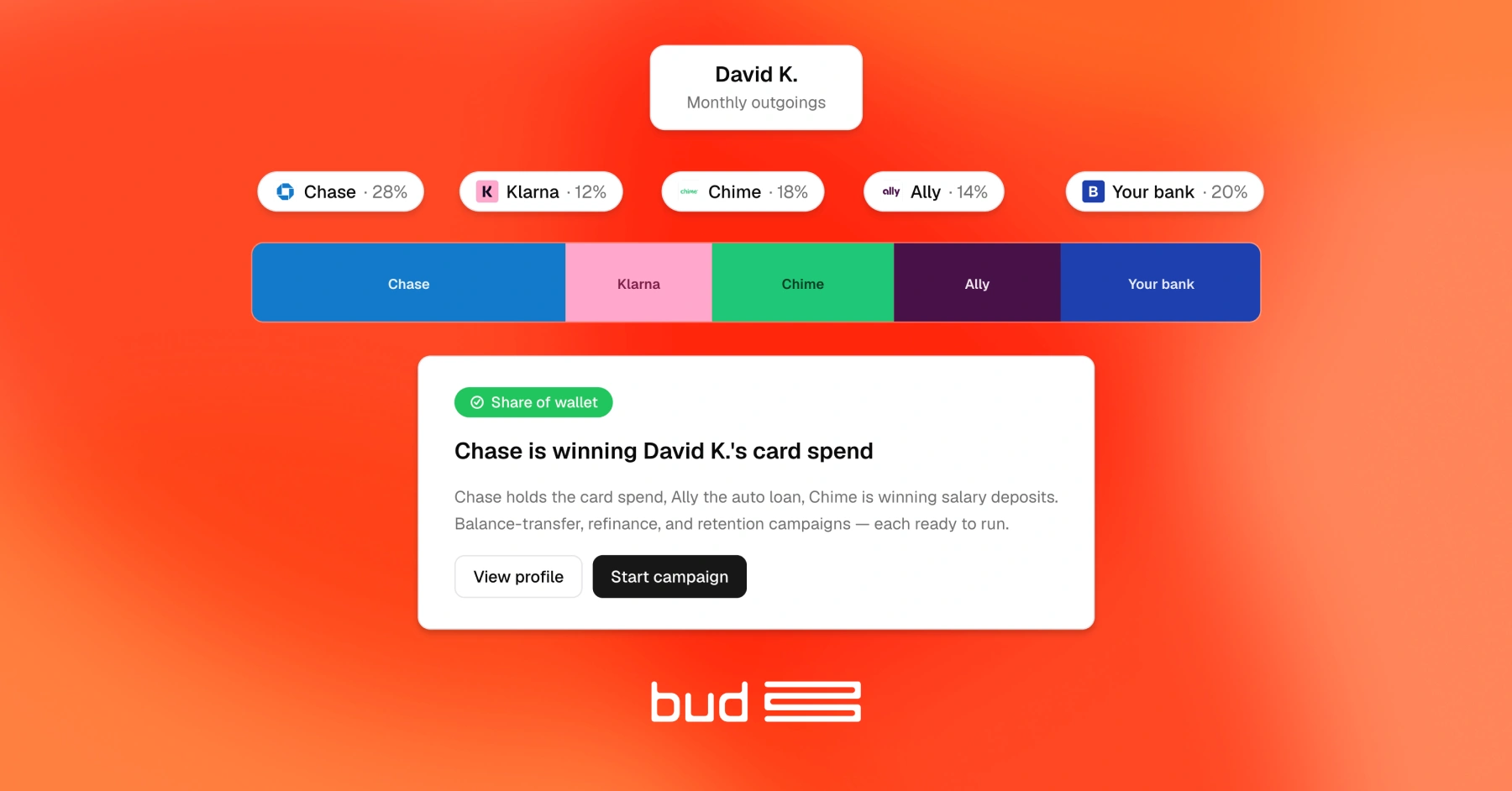

Open banking made your customers' other financial lives visible. The question is whether you can make sense of what you're seeing.

Generic transaction categories aren't enough. Knowing a customer has "loan repayments" is only a small part of the story. Knowing they're repaying a non-bank auto loan, holding a credit card with a named competitor, using Klarna and Clearpay simultaneously, and quietly moving their salary to a neobank — that's a picture you can actually act on.

Bud resolves open banking data into named provider relationships: specific card issuers, specific BNPL providers, specific banks and fintechs. That means your team can identify balance transfer candidates, refinance opportunities, and retention risks with precision, not guesswork. Share-of-wallet intelligence that used to require expensive third-party panels is now sitting in your own customers' consented transaction data.

None of this requires building new data infrastructure from scratch. The signals are already there, in the transactions your customers generate every day. The difference is whether you have the enrichment and intelligence layer to read them.

If you'd like to see how this works in practice, get in touch with the Bud team.

%201.webp)