.svg)

On Friday, OpenAI launched account connectivity and personal finance management (PFM) capabilities in ChatGPT for U.S. users. While this was always going to happen, it will (if not fumbled) accelerate the access to finance management tools for consumers.

At Bud, everything we’ve built centres around the idea that transaction data is one of the richest sources of consumer insight available. It provides deep context into peoples’ lives, habits, goals, and financial wellbeing. That’s why it’s exciting to see OpenAI recognizing the value of transaction data and beginning to incorporate it as context into their per-user “memory” to better understand and serve their customers through every interaction.

This signals a broader industry transition: financial experiences need to become more contextual, conversational and proactive, if they are to compete. We have already seen Revolut’s growth push the need for European banks to innovate more for their customers this year.

While many are not necessarily conscious of how powerful transaction data can be when used for context to things like serving ads, most consumers still do see transaction data as incredibly sensitive information. According to Bud research, over 3 times as many adults would rather use PFM / Insights in their banking app than a standalone app, and 5% of respondents said they'd switch banks for PFM / Insights1. Banks are the institutions consumers already trust with both their money and their data.

However, trust alone is no longer enough - when better financial experiences are offered elsewhere, consumers are willing to move both their data and attention. ChatGPT already having a massive daily active user base is likely to amplify this shift. Generally people want to use tools where they already are rather than get a new tool, but we know most people are using these tools daily and far more in Gen Z.

The implication for banks and financial institutions is significant: if customers can get smarter, more personalized financial experiences outside the banking app, engagement will naturally follow those experiences.

Great PFM experiences are built on a strong data foundation. Without high quality enriched transaction data, the whole analysis becomes unreliable.

Beyond having strong enriched data foundations, a modern PFM experience needs three core characteristics:

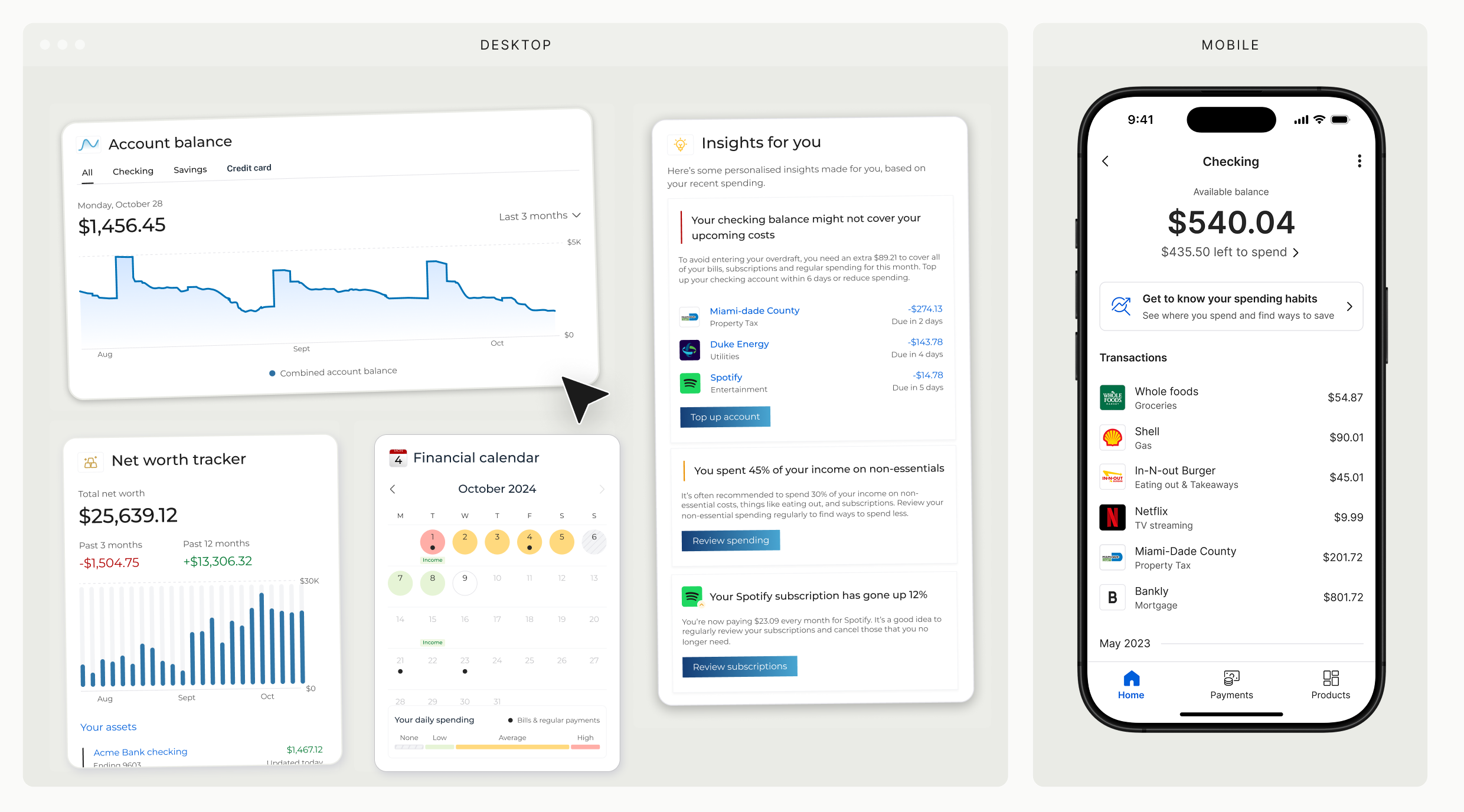

Consumers still need structured interfaces that help them quickly understand their finances. Dashboards, charts, lists, budgets and planning tools all remain important.

Historically, many PFM dashboards have struggled to create meaningful financial outcomes because they rely on static, one-size-fits-all experiences. But structured interfaces remain critical for repeated engagement and at-a-glance understanding, provided they intelligently prioritize what is actually relevant to the individual consumer.

The best experiences combine familiar UI patterns with intelligence underneath them. At Bud, this is why we use our Consumer Finances LLM to power smarter budgeting, financial planning and goal-setting experiences.

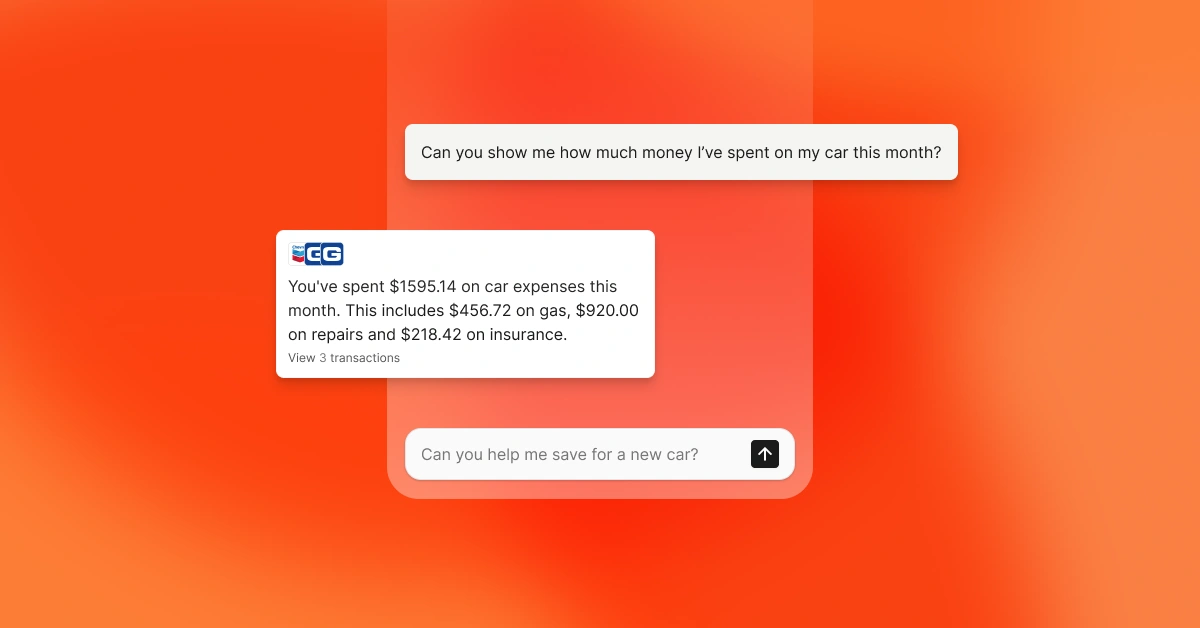

Consumers don’t always know the “correct” workflow for managing their money. Often, they simply have intent (“How much do I spend on my car?”, “How much did I spend on holiday?” or simply “Netflix”). That’s where conversational interfaces become powerful, and what OpenAI is doing very effectively.

Chat provides a natural way for consumers to ask questions about their finances while accommodating ambiguity and fuzzy intent. This is why we built Jas and Intelligent Search at Bud.

Jas enables broad conversational experiences, thought partnership and flexible financial workflows. Intelligent Search allows consumers to ask simple questions about their finances directly in the banking app, and instantly retrieve relevant transactions and insights with minimal AI-associated risk.

The combination of structured experiences and conversational flexibility is where truly useful PFM starts to emerge.

.webp)

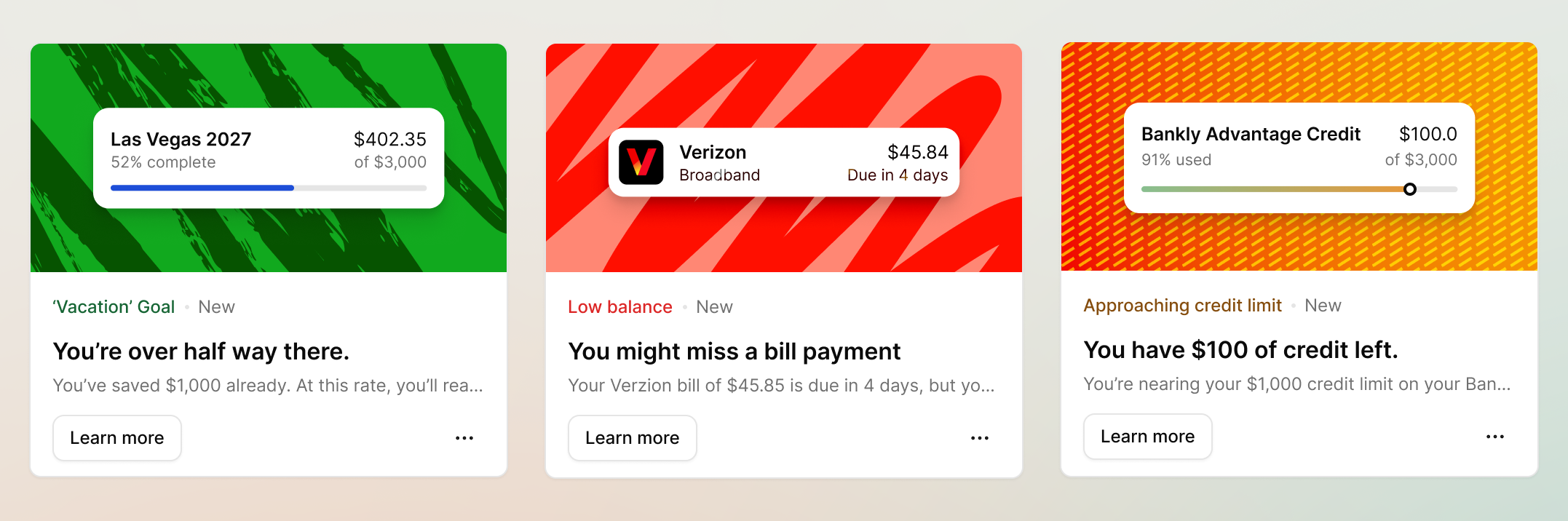

The biggest opportunity in PFM is not simply helping consumers answer questions. It is helping consumers before they even know which questions to ask.

Most financial tools today are reactive: users open the app, navigate dashboards, and actively search for information; or they go to a tool to ask it questions about what they can do to improve their finances. Great PFM works differently. It should proactively surface relevant insights, recommend actions, and help consumers improve financial outcomes without requiring constant manual engagement. This could mean:

OpenAI entering PFM demonstrates that they too believe in the power of unlocking financial data; and that consumers are looking for somewhere to give them smarter, more personalized financial experiences. The institutions that succeed will be the ones that combine high-quality transaction understanding, conversational AI, structured PFM experience, and proactive intelligence inside their own trusted experiences.

Banks already have the trust relationship and the data. The challenge now is delivering experiences that match rising consumer expectations.

Bud gives you everything you need to deliver that perfect PFM experience in the place where it works best and keeps engagement where you want it: your own experience. At Bud, we do it with the strongest foundation of underlying transaction understanding versus anyone else in the market (benchmark us and we’ll prove it). We build on that data layer with Bud’s Engage product that includes proactive insights, an AI chat for flexible powerful deep responsiveness, and a smart structured PFM experience for everything from financial planning to budgeting and spending analysis. After rolling out Engage one Bud client reporting a 50% increase in app engagement.

Contact the team today to find out how we can help you deliver best-in-class PFM to your customers, so they never have reason to go somewhere else.

1 Based on data from a YouGov survey

%201.webp)