.svg)

In a previous Bud breakdown article, we explored what transaction enrichment is and how Bud approaches it. We also looked at how enriched transaction data can be applied across a wide range of use cases within financial services.

However, transaction enrichment is only the starting point. While it transforms raw transaction data into something usable, it is ultimately a foundation for a more advanced and valuable layer within the platform: insights. At Bud, insights are not a single feature or output, but a system of interconnected data points that enable a much deeper understanding of customers and unlock a broader set of applications.

The Bud platform is designed to combine multiple sources of data into a unified view of the customer. This begins with financial transactions, but can extend to include CRM data, signals from digital and in-person interactions, and third-party inputs such as credit bureau data.

Importantly, these additional data sources are entirely optional. Transaction data on its own remains the most valuable and reliable indicator of customer behaviour, as it reflects real-world actions rather than inferred intent. This is why transaction enrichment plays such a central role; it acts as the primary input into all higher levels of insight generation.

For each transaction, Bud applies a range of enrichments, including categories, merchants, entities, processors, and locations. These labels make the data significantly easier to interpret and use, but on their own, they only provide a partial view of the customer.

The next level of insight comes from analyzing transactions collectively, rather than in isolation. By identifying patterns across multiple transactions, the platform begins to uncover how financial behaviour evolves over time.

One of the most powerful examples of this is recurrence detection. Bud can identify repeating transactions across any interval, rather than being limited to fixed timeframes such as weekly or monthly cycles. This flexibility allows for a more accurate and nuanced understanding of regular financial commitments.

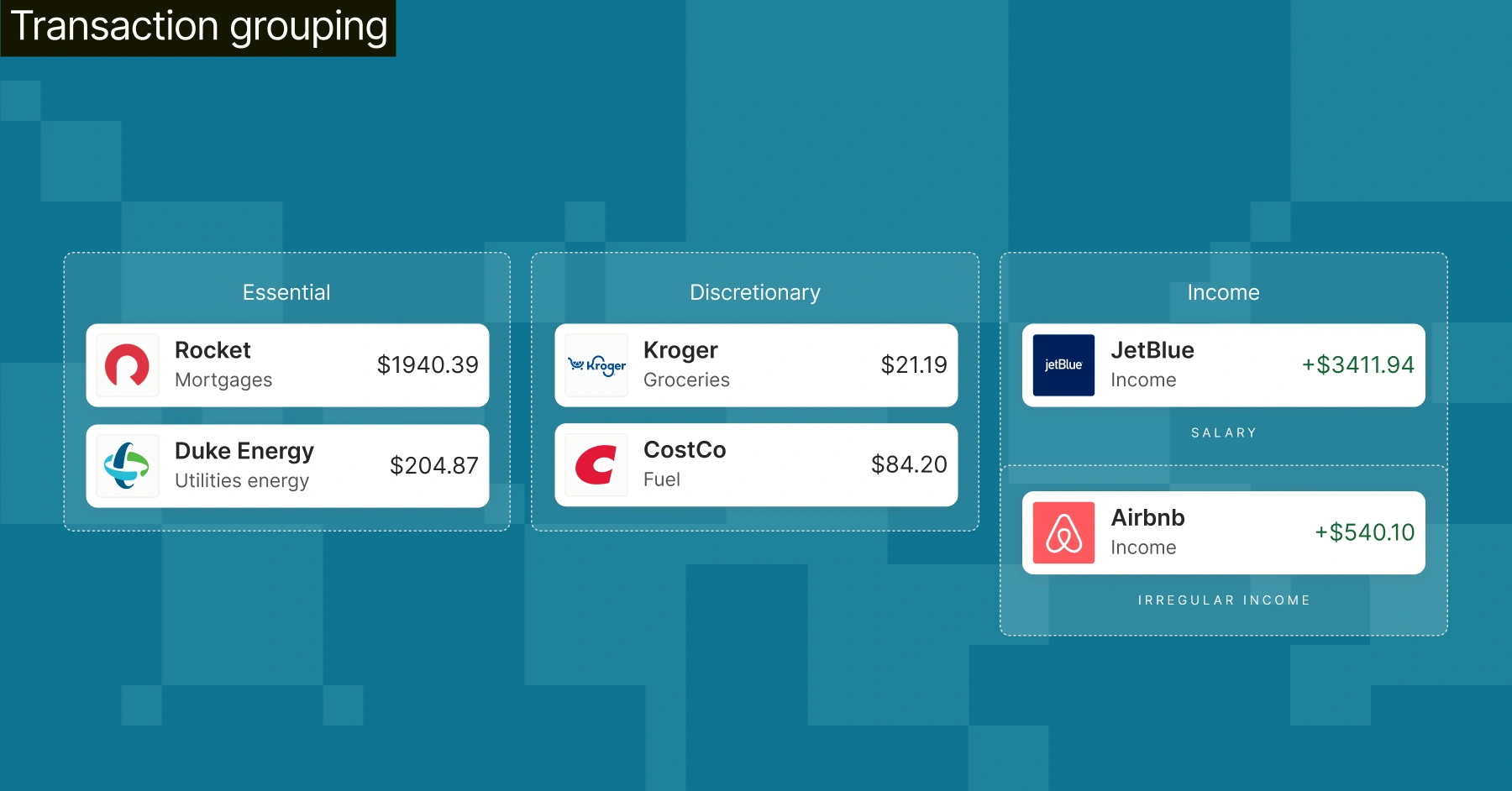

Beyond recurrence, transactions can be grouped in different ways to reveal additional meaning. Spending can be categorized into essential and discretionary, while income can be broken down into salary, bonuses, or irregular payments. These groupings help move from simple classification towards interpretation.

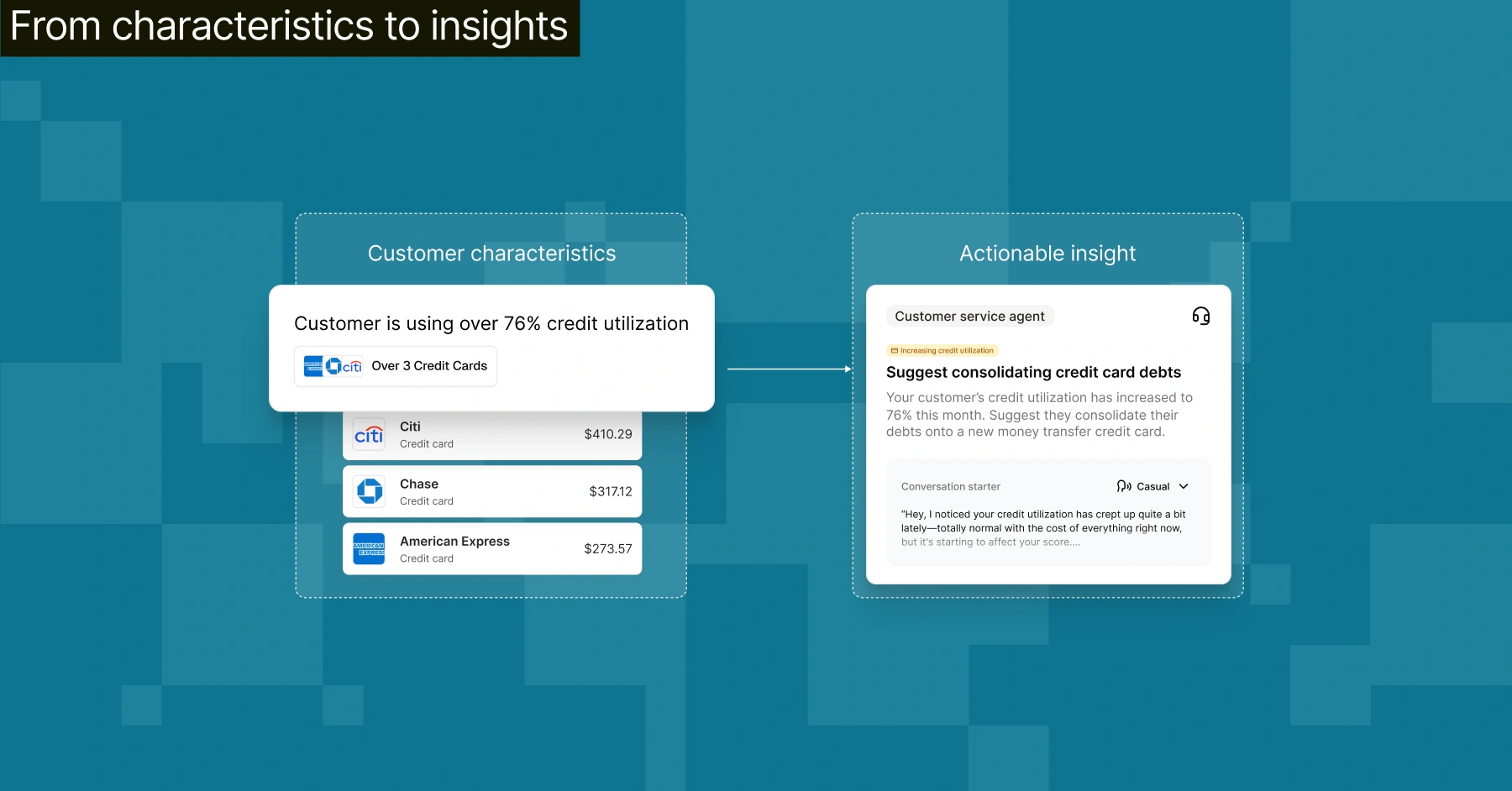

As these patterns are identified and refined, they begin to form what we consider to be facts about the customer. These are structured, explainable attributes derived directly from behaviour rather than assumptions.

Examples of these facts include income levels, the balance between essential and non-essential spending, or the presence of recurring expenses related to housing or vehicles. Each of these adds another layer of clarity, helping to describe the customer in a consistent and meaningful way.

This layer is critical because it bridges the gap between raw transactional data and higher-level decision-making. It provides a stable, interpretable foundation on which more complex insights can be built.

These behavioural facts become even more powerful when combined with additional data sources. Within the Bud platform, they can be layered with product data, digital engagement signals, customer-defined goals, external segmentation, and broader population-level information.

The result is a set of customer characteristics that can be used across multiple products and use cases. In Engage, these characteristics power real-time, customer-facing insights, helping to deliver relevant nudges, alerts, and recommendations at the right moment. In Drive and Focus, they act as building blocks for segmentation, targeting, and campaign execution.

This ability to unify different data types into a coherent set of characteristics is what enables a more complete and actionable understanding of each customer.

The true strength of the platform lies in how these different layers—enrichments, patterns, facts, and characteristics—can be combined. Rather than existing as separate elements, they can be dynamically linked to create more refined and context-aware insights.

Much of this process is automated. AI models analyse how different data points relate to one another and align those relationships with the organisation’s objectives. This allows the platform to move beyond static definitions and continuously improve the relevance of the insights it generates.

As a result, data becomes actionable. The platform is able to identify the most relevant next step for a given customer, whether that involves recommending a product, prompting a conversation, or triggering a specific piece of communication. This works both at a population level and at the level of individual interactions, such as when a customer engages with a digital channel or speaks to an advisor.

A large proportion of the insights generated within the platform are structured. These insights are clearly defined, built on traceable data points, and designed to be explainable. This makes them well suited for integration into external systems, compliance processes, and operational workflows.

However, not all insights fit neatly into predefined structures. For this reason, the platform also supports unstructured insights. These are more flexible outputs that remain grounded in data but are not constrained by rigid schemas.

Unstructured insights are particularly valuable when exploring new patterns or identifying emerging trends. They provide a way to surface signals that may not yet have been formalised, acting as a discovery layer within the platform. In many cases, once a pattern has been validated, it can be translated into a structured insight and scaled more broadly.

They are also well suited to generative interfaces, where flexibility and contextual understanding are essential.

For many financial institutions, the primary challenge is not collecting data, but extracting meaningful value from it. While transaction enrichment is an essential step, it does not, on its own, provide a complete understanding of the customer.

Achieving that understanding requires multiple layers of interpretation, moving from raw data through to insights that can directly inform decisions and actions. This is a step that many organisations have yet to fully realise, leaving a gap between the data they hold and the value they could generate from it.

The Bud platform is designed to bridge this gap by providing a flexible and scalable framework for transforming data into insights, and insights into outcomes. It can be deployed in a variety of ways, whether through APIs, end-to-end products, or integration into existing workflows.

The insights generated span a wide range of applications. Some are operational, supporting areas such as risk monitoring and compliance. Others are customer-facing, helping individuals better understand and manage their financial lives. Many are focused on growth, enabling institutions to identify needs, predict intent, and deliver more relevant engagement.

Ultimately, these insights shape the quality of every interaction. They make experiences more timely, more personalised, and more useful—ensuring that financial institutions are not just informed about their customers, but able to act on that understanding in meaningful ways.

Get in touch to explore how Bud turns transaction data into actionable customer understanding across segmentation, engagement, and decisioning.

___________________________________

Customer insights in banking are data-driven understandings of a customer’s financial behaviour, needs, and preferences. They are typically derived from transaction data, enriched with additional context, and used to inform decisions across engagement, product recommendations, and risk management.

Customer insights are generated by layering analysis on top of transaction data. This starts with enrichment (categorising and identifying merchants), then moves to detecting patterns such as recurring payments or income, and finally to creating structured facts like income level or spending behaviour. These elements can then be combined into more advanced insights.

Transaction enrichment focuses on making raw transaction data usable by adding labels such as categories, merchants, and locations. Customer insights go further by interpreting this enriched data to identify patterns, behaviours, and characteristics that describe the customer in a meaningful and actionable way.

Transaction data reflects actual customer behaviour rather than inferred or self-reported information. This makes it one of the most accurate and reliable sources for understanding financial habits, needs, and intent, forming the foundation for deeper insights.

Structured insights are clearly defined, explainable data points derived from transactions, such as income level or essential spending ratios. Unstructured insights are more flexible and exploratory, used to identify emerging patterns or trends that may not yet fit into predefined categories.

Financial institutions use customer insights to improve personalisation, drive targeted marketing campaigns, support financial wellbeing tools, enhance advisor interactions, and monitor risk. Insights help ensure that products, services, and communications are more relevant and timely.

Yes. While additional data sources like CRM or credit bureau data can enhance insights, transaction data alone is often sufficient to generate meaningful and actionable customer insights due to its depth and accuracy.

Insights enable financial institutions to tailor products, messaging, and recommendations to individual customers based on their behaviour and needs. This leads to more relevant interactions, better customer experiences, and improved engagement outcomes.

AI helps identify relationships between different data points, automate the creation of insights, and continuously improve their relevance. It can also align insights with organisational goals, ensuring that outputs are not just descriptive but actionable.

Segmentation groups customers into broader categories based on shared characteristics. Customer insights operate at a more granular level, providing detailed, individual-level understanding that can be used to inform segmentation as well as personalised actions.

%201.webp)