With access to millions of first party data points, banks and fintechs have the potential to help consumers take control of their finances, and better their financial position. Yet, in 2024, many customers are still starved of exciting, efficient and effective personal financial management tools.

The technology exists – and Bud’s data intelligence API capable of powering advanced personal financial management solutions and lay robust groundwork for those who want to build next gen financial wellbeing features or apps. Clients can use Bud’s Engage product to transform the financial lives of their customers, finding ways to increase engagement, grow share of wallet and reduce churn at the same time.

Thomas Purton, Senior Product Manager for Engage, explains what we mean by personal financial management at Bud, and shows how Engage can pave the way for financial resilience in a time dominated by uncertainty.

What is personal financial management?

The term personal financial management (PFM) describes the online tools and digital banking solutions that empower customers to make better financial decisions. There are many PFM providers, each with their own application or API.

These PFM tools can have a significant impact in long-term financial planning, retirement planning and day-to-day budgeting.

However, Thomas tells us that traditional PFM has often been underwhelming for both the banks and their customers: “Historically PFM features required extensive manual work in order to set up and understand the data. This in turn created a barrier to entry for consumers which meant that adoption rates have been lower than anticipated.

“From what we’ve seen,” continues Thomas, “some banks are providing a random PFM feature within their banking app without providing an explanation or prompt of how the customer can use it to improve their financial wellbeing.”

For example, financial institutions that don’t have access to an individual’s transactional data have previously been forced to make assumptions based on age, location and product holdings. But creating customer segments based on these assumptions often leads to generic messaging that doesn’t resonate with customers.

Thomas explains: “Imagine sending notifications for home insurance products to a customer who doesn’t own a home. They don’t care about home insurance. On the flip side, a deeper understanding of your customer’s data allows banks to tailor a product to their customer’s current situation:

“Hey, we’ve seen you’re paying a mortgage, but we can’t see any payments relating to home insurance. Here’s some information about our home insurance product.”

Consumers without access to PFM tools are often left to make sense of the data themselves, without support or training. Setting an arbitrary day of the month to pick through transactions and export it all to a spreadsheet, consumers can feel like their time has been wasted.

The frustrations only mount up further on the realization that other banks are offering financial wellbeing solutions in app – and customers can go on to question if your bank is the right choice for them.

What is Engage and how does it work?

There are three steps to make sure that money management software helps customers enough to ensure participation and true benefit:

- Enriching customer transaction data: understanding spending through categorization and merchant identification.

- Educating the customer: enabling the customer to recognize poor financial habits and how to make progress with finances.

- Encouraging action: prompting a change in financial behaviour.

Engage is Bud’s suite of PFM tools and its data enrichment is underpinned by core models: categorization, merchant identification and regularity.

Thomas notes, “If you don’t get data enrichment right, then all of the following developments will also be wrong. At Bud, we are a market-leader in enrichment, so any of the subsequent PFM tools clients build are likely to be more accurate and therefore more useful for consumers.”

Why is Engage crucial for forward-thinking financial services providers?

Without a focus on this core technology, financial institutions will find it difficult to gain the initial intelligence required to educate customers about their own financial lives. Then, it becomes almost impossible to recommend or prompt the next course of action with any level of personalization.

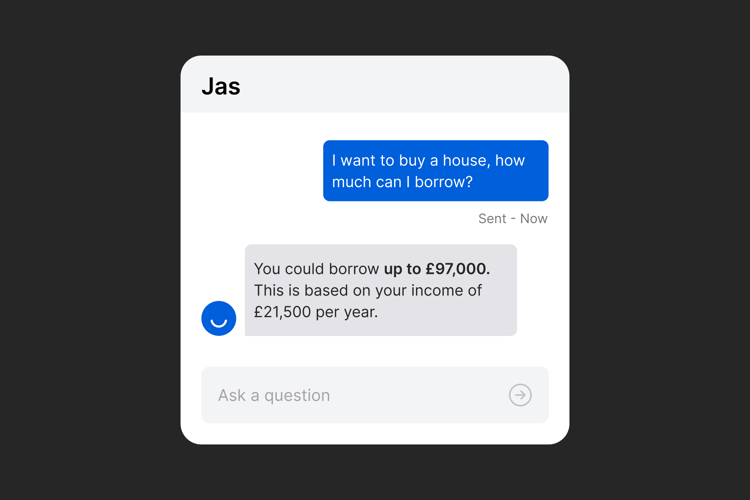

Engage’s spending insights feed into personalized engagement for the customer through the creation of customer journeys. For example:

“Hey, we can see (based on your transactions and savings goals) that you might be saving for a wedding.”

By identifying a customer's financial aspirations, clients can then educate them into taking the next step, whether it be moving savings into a higher-interest account, or suggesting a credit card with travel rewards for the honeymoon. It’s Bud’s superior data intelligence that allows the automation of this process. “Engage is redefining the personal financial management space because it combines both education and action – generating the biggest value add for both customer and financial institution,” says Thomas.

What are the benefits of Bud’s PFM API, Engage?

A customer-centric product, designed to transform the financial lives of your customers, Engage works to:

- empower customers with actionable insights

- foster mutually beneficial relationships between financial institutions and customers

- reduce the cost of customer acquisition

- innovate towards a financially literate and engaged society

- improve customer creditworthiness and value.

Empower customers with actionable insights

The actionable insights gained from Engage give customers the opportunity to build financial resilience, for example:

“Hey, we can see that you’re trying to save for a vacation because you’ve set up a vacation savings goal. Would you like to switch on the roundups feature? If so, we’ll automatically round up all your spending and add it to your vacation savings pot.”

For customers, this type of hyper-personalized advice not only works to help build savings faster but also ensures they are less likely to take out short-term loans or pay interest to other financial institutions. This greater financial resilience across customers is also beneficial to financial services providers as it leads to an increase in the total amount of customer deposits – and therefore revenue and ROI.

Thomas notes how this example is relevant to the current macroeconomic conditions:

“For the first time since 2008 the federal funds rate, is above 2%. So there are millions of people who have entered the world of work, and never been incentivized to put money into a savings account. Suddenly, it’s within their best interest to do so – and institutions are now interested in how to encourage customers to move money into their savings accounts”.

Financial institutions can use Engage to identify the customers with ‘lazy’ money in their current account, that’s not generating any interest. Then, using insights from Bud, they can educate their customers, and encourage positive financial actions. This helps customers to make their money go further.

And to take it to another level, you could even combine Engage with our latest AI-powered data intelligence solution, Drive, for supercharged data exploration business-wide. With Drive, you can identify relevant customer segments and send personalized recommendations with ease – empowering them to make data-driven financial decisions at the right time, every time.

For you, this means increased deposits and product holdings, greater satisfaction and improved customer loyalty.

Foster a mutually beneficial relationship between financial institution and customer

When institutions access real-time customer transactional data via Bud’s platform, they can make better decisions for both the business and their customers.

A use case for Engage, often considered the most important by institutions, is its ability to help increase wallet share.

“Hey, you’ve got £650 sitting in a 0% interest current account that you don’t seem to be using each month. Would you like to move it into a savings account with us, where you can earn 4% interest? This could equate to £26 over the course of a year.”

For the customer, this is clearly advantageous. But, Thomas explains, financial institutions can benefit from increasing customer deposits, leading to greater lending potential (and better interest rates).

“Institutions might offer 4% for savings, but expect 6% on loans – charging a borrower to have the same money. They’re essentially making 2% on all of the money that a customer deposits into the bank,” he says.

Reduce the cost of customer acquisition

A further benefit of Engage is that it facilitates a digitally-native customer experience. Bud has learned that there’s a correlation between strong digital experiences and customer recommendations.

One of the best ways to reduce the cost of new customer acquisition, then, is to encourage more recommendations by delighting the customer with the digital app experience. If successful, this can be more cost efficient than pumping millions into the annual marketing budget.

Thomas explains how Engage can better the digital experience at the core of the program: “It’s really about creating this visibility over the customers’ financial life.

"For example, if they would like to see all of their active subscriptions, it’s as simple as using Bud’s subscription finder endpoint. Then, we can display every single subscription the customer has coming in and out of their account, making it much easier for the customer to review, and then take action to cancel any redundant services.”

Innovating for a financially empowered society

It’s ongoing innovations in PFM that are setting the stage for a financially empowered society. For example, with consumer-centric solutions that work, customers can reach their savings goals faster, move away from high-interest short-term loans and build towards a stable financial future.

Financial institutions are using Engage to achieve their financial plan and it’s the upselling and cross-selling channels that are seeing the most success. In a recent study (in collaboration with an independent third party), Bud found that personalized product offerings make customers twice as likely to engage, and three times as likely to engage for customers under 44 years old.

Here’s one example of how Engage PFM features enable clients to upsell and cross sell with confidence:

“Hey, we’ve seen that you’ve been looking for a credit card. Based on your average income and expenditure, you’d be pre-approved for this type of credit card with us, which can offer the following benefits. Would you like to apply?”

So, clients looking to bolster their own PFM offerings should focus on learning as much as they can about customers first. This enables clients to provide services such as:

- Savings goals

- Spending budgets

- Personalized product suggestions

Each of these services provides an automated alternative to time-intensive and manual finance tracking within a spreadsheet or elsewhere. It’s also beneficial because it helps customers to visualize their finances, which can make the second step, financial education, much easier to digest.

How are PFM tools transforming financial futures?

The transformative potential of personal financial management cannot be understated.

Without a data-oriented approach, customers become easily overwhelmed by scores of product offers that are constantly fired over. By inundating consumers with irrelevant marketing messaging and driving brand fatigue, customers will be less likely to open your emails or push notifications, let alone convert.

Instead, solutions such as Engage, encourage businesses to act with optimal efficiency. Intentionally targeting key customer segments with utmost precision, institutions can deliver the products that fit the customer exactly where they are within their financial journey.

Embrace the future of personal financial management with Bud

Limited resources are likely to put a dampener on banks who have the grand ambitions to develop personal finance tools internally.

That’s where we come in.

Priding ourselves on the simplicity of our API implementation, Bud specializes in working with enterprise banks and fintechs, each with their own use cases and data preferences.

Embrace innovation and benefit from the experience we’ve gained through nearly a decade of transactional data intelligence, plus more than 2 billion enrichments (and counting) by partnering with Bud today.

Interested in learning more about Engage?